If you own a small business and have ever needed financing, chances are that at some point you’ve turned your gaze towards an SBA loan. Whether you are seeking to finance an existing business, or to purchase a new one, an SBA loan can be an attractive option.

This is particularly true if your bank turned you down because you had insufficient collateral, as that’s the one area where the SBA excels: lending to businesses with good cash flow, whose owner have good personal credit, and experience, but insufficient collateral.

There are plenty of resources online that get deep into the weeds on all the SBA loan requirements, features, and pros & cons, so I’m not going to regurgitate all that.

Instead, I want to discuss just one additional feature that is seldom mentioned because it’s a feature that most SBA loan originators don’t have experience with. What happens if your venture fails, and you’re on the hook for the balance of that loan that seemed so attractive a year ago? This is where the SBA Offer in Compromise comes in.

Before we delve into the wonderful world of Offer in Compromise, there’s one tidbit to remember: the SBA is not a direct lender. They simply guarantee the debt so that in the event of a default, the lender is reimbursed for a portion of the loan.

What Exactly Is An Offer In Compromise?

Commonly referred to as an “OIC”, Offer In Compromise is the SBA’s term for a settlement. In exchange for cash payment, either via lump sum or installments, the SBA will consider releasing borrowers and guarantors from liability for less than the balance owed.

Let’s be clear: The OIC is a last resort. In order to qualify, things need to have gone terribly wrong. In the vast majority of cases, the SBA won’t even look at an OIC unless the business has ceased operations (selling as a going concern is ok too), and all the business assets have been liquidated.

The SBA will never settle for the sake of settling. Over the years, I’ve had borrowers reach out to me ask if there was a way to dangle a payoff in exchange for a discount. In my experience, that’s a non-starter for the SBA.

Why Would The SBA Settle?

Everyone is familiar with the term “cut your losses”. That’s exactly the thought process that the SBA has when it comes to salvaging defaulted loans. When a business closes, taking the entrepreneurs investment with it, the bank is often left with an outstanding loan balance that simply can’t be repaid. You certainly know it, and they know it too.

When a guarantor is personally liable for $100K, $500K, or $1 Million, the chances of full repayment is, in most cases, slim. They’ve already plowed their savings even their retirement into the business, so any offer will amount to but a fraction of the outstanding loan balance.

In these cases, the SBA has a decision to make. Stick to the unrealistic notion of full repayment, or accept reality and settle for a lesser amount. To their credit, the SBA understands that $50K in hand is worth more than a $500K judgement against someone who clearly doesn’t have it.

Who Actually Approves An OIC?

There some nuance, but the key fact to know is that the SBA always has the final say. If a bank consummates an OIC without SBA approval, the lender runs the risk of a partial or complete loss of SBA reimbursement (known as a “repair” or “denial”).

If your original lender is servicing the loan, an OIC needs to be recommended for approval by the lender. As a practical matter, this means you need your lenders support. Going over their head typically goes nowhere, so be sure to play nice in the sandbox with your lender. This means being forthcoming with information, and promptly responding to call and emails.

Can All SBA Loans Be Settled?

No. The OIC process is reserved for situations when there is a lack of collateral, and the obligors (borrower and/or guarantor) lacks sufficient resources to repay the loan in full. No free rides here.

An OIC is unlikely to be approved if:

- you’ve pledged your home, and it has sufficient collateral to repay the debt.

- you have personal assets such as savings, investments, or real estate that, if liquidated, have sufficient value to pay off the loan.

- your monthly income would allow you to continue to make monthly payments, or borrow from another lender to pay off your SBA debt.

How Much Will The SBA Settle For?

Ah, the million dollar question. Although in this case, I suppose you could call it the “I certainly hope it’s not a million” dollar question. The SBA doesn’t have any specific requirements in terms of dollar amounts except for a minimum of $5000 (except in cases of extreme hardship). Rather than focusing on a specific dollar amount or percentage of the amount owed, they really want your offer to clearly represent the most that you can afford.

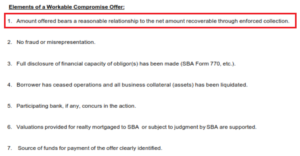

“The most you can afford” can be subjective, so to make a little clearer, the SBA instructs lenders that a workable compromise offer should bear a reasonable relationship to the amount recoverable through enforced collection. That’s jargon for “what could they get if they sue you, obtain a judgement, and collection on that judgement?”

This All Sounds Stressful and Expensive. How Is This This A Positive Feature?

It’s not a free pass by any means, but the OIC process is fair and consistent. Considering that many non-SBA lenders go straight to litigation when a borrower defaults, I’d argue that the SBA OIC routinely saves people from taking the drastic step of filing for bankruptcy. If you plan to borrow again for any reason, anyone who’s ever tried to borrow with a recent bankruptcy on their record will tell you how hard that will be. So while it’s not the scenario that anyone hopes for, the OIC might just be the one SBA loan feature that enables you to live to fight another day.