Following SBA loan default, you will probably not ever qualify for an SBA loan ever again. Hurt me once, shame on you. Hurt me twice, shame on me. That’s the SBA’s fundamental stance on lending to a borrower who has already failed to repay any federally subsidized loan.

Let’s go into the weeds to explore the reasons why you probably won’t have a chance to default twice on an SBA loan. One of the lesser discussed consequences of SBA loan default can be credit impact and/or inability to qualify for federally-subsidized programs in the future.

Personal Credit and SBA Loans

SBA loans are a great option for people for whom a regular commercial loan is not possible.

One major misunderstanding about SBA loans is that they are NOT for people who have bad credit. Just like any cash flow lender, SBA lenders don’t want to lend to people who have a spotty history of repayment.

Common scenarios that are perfect for SBA loans are business purchases where there is insufficient collateral. Unlike their hesitations about lending to people with bad credit, the SBA is willing to lend due to a lack of collateral.

Why Do Banks Care So Much About Personal Credit?

When I see advertisements for credit repair, I wonder who their typical client is. Is it a person who has some errors that need fixing? Or are they people haven’t repaid their debts, and now can’t get a loan? I hope it’s the former. Because someones credit history is actually really telling, and shouldn’t be altered to change facts.

When people owe me money, they are typically one of two types:

- The first type tells me they will pay, then they never do. I follow up, and I get some sort of excuse. The check is in the mail. They are waiting for money. They are travelling (as if cell phone reception ceases to exist anywhere outside their home). I even had one guy tell me that he didn’t have the money because, and I wish I were kidding, he was day trading stocks because he didn’t have enough to pay the SBA settlement. These people keep living their life, spend however they wish, while I wait to get paid. These people make me crazy, and dealing with it is definitely the worst part of my business.

- The second type of person tells me they will pay, and they do everything they can to make it happen. They are easy to reach, often even reaching out to me to let me know where things stand. These people prioritize their financial commitment to me. I don’t worry about these people.

So what’s my point?

The point is that some people care deeply about honoring their financial commitments, and other simply say and do whatever is necessary to allow them to put off paying another day. That matters to me, and it definitely matters to lenders. The credit report tells a story. Are you the type of person that finds a way to honor their financial responsibilities, or do you make excuses about why you can’t?

Are there exceptions and extenuating circumstances? Sure, and many lenders will consider them. But in general, a persons credit report will tell you exactly how this person handles their finances.

Will SBA Loan Default Hurt My Credit Score?

I’ve answered this question before here. But it bears repeating, especially since things are always changing.

Here’s the deal with your credit and SBA loan default. Most banks, in my experience, don’t report personal guarantors or borrowers (if the borrower is a person) to credit bureaus. So if your bank does not report your loan to the credit bureaus, going into SBA default won’t trigger any particular credit event.

If the bank does report to the credit bureaus on the loan, then yes, a default will show up on your credit.

Other circumstances that may result in your defaulted SBA loan showing up on your credit:

- If the lender gets a personal judgement against you, that will likely show up on your credit report.

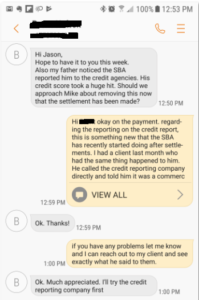

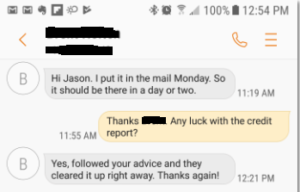

- If your file is referred to the SBA, and we negotiate an SBA offer in compromise directly with them, they may report it to your credit. I recently had 2 clients that both settled with different SBA offices. Soon after, their settlements were reported on their personal credit.

Luckily, both clients were successful in getting these items removed.

Can I get another SBA loan in the future after I default?

As I said in the first sentence of this article, probably not. The government is pretty adamant that if you fail to repay them, they aren’t going to get burned twice. And it’s not just SBA loans, this applies to HUD loans, FHA loans, student loans, and VA loans.

The government keeps a list of all the people who have defaulted on various government-backed loans. This list is most commonly known for the acronym CAIVRS. It’s actual name is Credit Alert Interactive Verification Reporting System.

It’s important to keep in mind that a settlement is not the reason you end up on CAIVRS. Failing to repay the debt in full is the reason you end up on CAIVRS. The only way to get off CAIVRS, I hear, is to repay the debt in full. I’ve read in some places that you may be eligible to come off the list after 3 years, but I’ve not been able to verify whether this is accurate (sorry, I don’t know everything!). You may be able to ask SBA for a waiver, but again, I have not actually seen this in action, so I don’t know the likelihood of success. My gut says slim to none.

Fine, forget SBA loans. What about other types of government subsidized programs?

You’ll probably be disqualified from other programs too. I’ve gotten many calls from people who have applied for FHA loans, VA loans, and certain student loans, only to be rejected as the result of an SBA loan default. Sorry, Charlie. CAIVRS will follow you.

When people call me with this issue, they of course want to know how to get off the list. I only know of two way: you can ask for an exception or you can repay the debt in full.

The point I always make to people is that while it would be great to have an FHA loan, in many cases it would not be worth it. The cost to repay a $600K loan would far exceed the benefit of an FHA.

Will I ever again qualify for another business loan?

You can, but it may have to be a traditional commercial loan and not an SBA loan.

Let’s talk through the scenario. If you apply for an SBA loan and good old Mr. CAIVRS rears his ugly head due to your SBA loan default, it’s not necessarily game over. If your SBA lender (the one you defaulted on) didn’t report to the credit bureaus, there’s nothing that says a traditional bank loan won’t be an option. You probably want to apply for that loan with a different lender than you took the SBA loan from (duh!).

Final Thoughts

While it’s true that you won’t be able to get another SBA loan (or HUD, VA, FHA and student loans for that matter), it usually doesn’t mean that you won’t ever be able to borrow in general. And while it may not be fun to admit, if you failed to repay the SBA or other creditors, but by not lending to you in the future they may actually be doing you a favor. Dealing with SBA loan default, after all, is no picnic.

Do you have more questions about the SBA Offer In Compromise process? Read my Definitive Guide To SBA Default and Offer In Compromise.