Don’t feel like reading? I’ve turned this article into a Podcast Episode:

If you want a summary of the entire SBA loan default and SBA Offer In Compromise, check out my Definitive Guide To Offer In Compromise.

“Hi Jason, what can happen to me if I can’t repay my SBA loan?”

Hello, made up caller, and thanks for reaching out! While this article is fictional, it’s based on all the actual conversations I’ve had over the years. To make this orderly, I’m going to talk about consequences that this writer would characterize as the major downsides of SBA default. Said another way, these are the things that would keep me up at night if I an SBA borrower.

1) You could lose your home

In a worst case scenario, a bank could foreclose on your home, then apply the proceeds to your loan balance. Will you lose your home? It depends on a number of factors:

A) Is there equity in your home?

Back in 2008 (over 10 years ago, can you believe it?), when the economy was in shambles, home values across the country were dropping like stones in a pond. In California in particular, property values were dropping 50% or more. When borrowers first took their SBA loans, their home worth was $1 Million, and they owed $600,000 on it. After the economy crashed, that home was now worth $600,000. Poof, no more equity. As a result, we were settling many SBA loan defaults and getting homes releases. Even if the debt wasn’t settled, do you know what the bank would not be doing? Foreclosing.

B) Is your home pledged as collateral?

Many people confuse the personal guarantee with a lien (sometimes known as a Deed of Trust). For the record, they are not the same thing. Just because you gave a personal guarantee doesn’t mean you also granted a lien on your home. And the distinction is important, because going after someone’s property is much more difficult when there is NO lien. And in most cases, even a personal bankruptcy won’t get rid of the lien. If you didn’t give a lien? A personal bankruptcy will probably keep your home out of the hands of your lender.

C) Do you have a large mortgage (or mortgages) ahead of the SBA lien?

Not all equity is created equal. If your home is worth $500K, and you owe $200K, you have $300K in equity. If your home is worth $2 Million, and you owe $1.7 Million. Again, $300K in equity. So even though both homes have the same amount of equity, one is a much more desirable scenario for a bank. The reason is that in the second scenario, the bank would have to “invest”$1.7 Million to chase $300K. This is not a desirable scenario for the bank. If the price dips even 10%, the bank could be looking at recovering very little in the way of cash.

D) Is your bank a bunch of jerks? Jerks are everywhere, and it’s unfortunately luck of the draw sometimes.

I worked for a lender who would start foreclosure on a property even if there was no equity in a property, then call it off at the last minute. That’s hard core. And a waste of legal fees, in my opinion. And kind of jerky thing to do.

2) You could have your bank accounts and investment accounts wiped out (aka levied).

If the bank successfully obtains a judgement against you, they could levy your bank accounts. I once had a client call me in a panic because the bank took $50K out of their account. We were in conversations with the bank about an OIC, but the bank went ahead and did it anyway. We know it was a possibility because of the fact that the bank already had a judgement (fortunately this is not common – most files I am involved with never make it to litigation), but were surprised that they would do such a thing, since we thought we were working in good faith.

The really terrible thing about getting your account levied, as compared to an OIC, is that even after they clean out your bank account, you’ll still owe the remaining balance. In other words, if you owe $500K and they sweep $50K out of your account, you’ll still owe $450K. Compare that will voluntarily offering $50k to settle.

In either case, you’ll end up parting with your cash. While that part stinks, wouldn’t you rather it be over and done with? Of course! This is precisely why want to negotiate an OIC immediately following your SBA default.

3) You could have your wages and social security (if it still exists when you are eligible) garnished.

Nothing is as unpleasant as getting a notice that you are going to have 15%-25% (it varies by state) of your paycheck taken. Once that happens, you are kind of stuck unless you change jobs or file for bankruptcy. I even had an attorney tell me once that even after personal bankruptcy, the SBA still may be able to garnish social security.

One of the most common calls I get is from people who have received notice from their employer that the US Treasury is going to start wage garnishing their paycheck. If I get that call, it’s usually too late. Once they start garnishing, they are like a pitbull. They sink their teeth in, and don’t let go. If the Treasury is taking $500 per paycheck, that’s $12K per year or $60K over 5 years. Do you think at that point they’ll be interested in taking your settlement offer of $10,000? Hint: nope.

Once wage garnishment starts, there are only a few ways to stop it. None of them are easy, or in some cases, even within your control:

- You stop working at that job. The bummer of that is even if you get a new job, it’s only a matter of time until the garnishment starts up again. As you probably know, every employer sends a copy of your W-2 to the Treasury annually, so quitting your job is not a permanent solution to your SBA wage garnishment problem.

- You file for personal bankruptcy. If you don’t owe the money any more due to a bankruptcy discharge, wage garnishment goes away.

- You settle with the Treasury. If you can successfully settle with Treasury, may I also suggest that you play Powerball too? The odds of settling are roughly the same for most people. The only difference is that Powerball is much easier to play on account of the fact that they don’t rely on fax machines and long phone holds as their main methods of communication.

- If you were fired from a previous job in the past 12 months. Apparently they won’t settle for a reasonable sum, but if you were fired from a job, they have a soft spot for that. Go figure.

4) You probably won’t be able to get another SBA loan, or federally backed loan.

The federal government essentially keep a blacklist called CAIVRS. If you fail to repay any loan that is guaranteed or subsidized by the federal government, they don’t want to get burned twice. When I worked for CIT (the largest SBA 7a lender at the time), I heard there was a guy in NY who took an SBA loan, then promptly defaulted. And then a few years later, this same guy relocated to Florida, took another SBA loan and defaulted on that one too. For obvious reasons, the SBA wanted to make sure that sort of thing doesn’t happen again.

To be clear, regardless of whether you settle or don’t, the chances of getting another SBA loan in the future are not good. The act of settling is NOT the reason why you won’t qualify for an SBA loan in the future. The reason you won’t get another SBA loan is because you failed to repay the debt in full.

If you don’t repay the loan and successfully negotiate an OIC: you won’t get another SBA loan.

If you don’t repay the SBA loan and don’t settle the SBA debt: you won’t get another SBA loan.

So when you are considering whether you want to pursue an OIC following your SBA loan default, you probably won’t be getting an SBA loan in the future either day if it’s clear that full repayment isn’t an option, so that shouldn’t really be a consideration.

5) You will lose your entire investment in the business, and the SBA won’t care.

When I work with a client to prepare the SBA 1150, the client often wants to convey how much money THEY lost as a result of this default. Every time this happens, I caution against it.

The SBA loan is debt, not equity. This means that when things go gangbusters for your business, the lender doesn’t participate in the success. Along similar lines, when things go wrong, the lender isn’t interested in giving you “credit” for your equity contribution or past loan payments. Whether you put $100,000 of $1,000,000 into your business, this will not be the focus of your SBA workout officer. Again, their focus is not on what you lost, but rather, how much you have left to pay them.

There’s only one reason I can think of that the loss of your investment might matter to your bank or the SBA. If the investment represented depletion of your personal assets. So if you put $250,000 into the business, and that represented 99% of your personal net worth, that will be considered because it means your resources are limited.

Borrowers often want me to let the bank know how much had been repaid on their defaulted SBA loan. “If you include the interest I paid since I took this SBA loan”, they reason, “then they’ve actually gotten all their money back!” While I understand where you are coming from, banks don’t look at it that way.

Obviously, banks are in business to make money. Collecting interest on their principal is typically a bank’s main source of income. So, at no point will your lender say “we made plenty on this borrower, so I’ll cut them a break”.

The bottom line is that regardless of how much you lost, you should not expect to get any brownie points or credit for it.

6) If you want to settle, you are going to need to crack the piggy bank open.

Many borrowers initially believe that the Offer In Compromise solely consists of the liquidation of the business or business assets. They are shocked to learn that business liquidation is only step one. Just for the record, if you hope to successfully settle your personal guarantee, it will require you to fund the settlement from your personal assets. This means cash savings, borrowing against or selling real estate, and even tapping into retirement accounts (not required, but often is the only option to raise cash).

7) You may have to spend lots of time and effort, but get nothing out of it.

When I worked for CIT Small Business Lending (was actually sold to Readycap Lending) we had a borrower who was able to find a buyer for his business. Yahoo, right? Until the business owner refused to close the sale unless his personal guarantee was released as well. Not a bad idea, unless you know how the process works. The SBA will not entertain this type of approach. The business owner dug his heels in, thinking the bank and SBA would cave. Of course, they didn’t. And the deal fell through. The lesson here is that while it will reduce your loan balance, the time and effort you spend to sell your business will not get you much other than a “thanks”.

8) Your landlord will have their hand out.

Your lease and your SBA loan are often your two largest obligations. While you may not think of it this way because rent is a monthly payment, multiplying your rent times the length of your lease will often exceed your SBA loan balance. Be prepared to negotiate with your landlord just as with your bank and SBA.

Thanks for the uplifting article, Jason. Are there any silver linings here?

Sorry, I don’t mean to be the bearer of doom and gloom. Obviously SBA loan default is no picnic, but what I wrote above are the theoretical worst case scenarios. I wrote about them because honestly, that what people always ask about.

Asking about the worst case scenario is perfectly natural. When things are going poorly, my mind certainly goes to “ok, so how bad can it get?”. But keep in mind that in most cases, all of the above are not likely to happen to you. Especially when it comes to losing your home, having your bank account levied, or your wages garnished.

While what I wrote is possible in theory, now I’ll tell you my experience with home foreclosures, bank levies, and wage garnishment in the real world:

A) Your Home

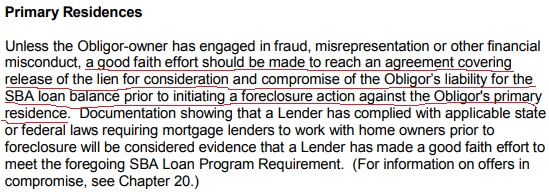

When it comes to your home, the SBA specifically encourages lenders to attempt to find a mutually agreeable resolution. They don’t want banks kicking people out of their homes. Below is a screenshot plucked directly from the from the SBA SOP.

I’ve negotiated many SBA lien releases (note: the lien is usually not placed by SBA, but by the bank who originated the loan). I can tell you that a successful SBA lien release is far more common than SBA foreclosure. I’ve been at this SBA loan default thing for almost 10 years, and can tell you that I’ve seen far more successful releases than foreclosures.

Please note the first sentence in the screenshot above. If you’ve engaged in fraud or misrepresentation, the SBA may no longer willing to be so humane when it comes to foreclosing on your home. Consider that when someone tells you to sell your business to a friend or create a new LLC, then take it back later. There’s no way someone could, in good conscience, claim that such actions are not clearly misrepresentations.

B) Levy of your bank or investment accounts

I can’t speak for all SBA loan default situations, but when I get involved, there is usually no judgement or garnishment of bank or investment accounts. The key is to proactively work with your SBA lender to reach a mutually agreeable resolution BEFORE it reaches the. Do you know why banks usually refer defaulted SBA loans to their SBA attorney? Because the borrower is either uncooperative or unresponsive, and they believe it’s their best chance at a recovery. On the flip side of that scenario, if you provide full disclosure, don’t do anything shady, and submit a reasonable SBA Offer In Compromise, the lender won’t need to refer it our for legal action.

C) Garnishment of your wages or social security

The most common situation where wage and social security garnishment comes into play is when the file gets referred to the US Treasury. While the file is with the bank or SBA, it actually doesn’t happen that frequently (again, I can only speak to situations that I’m involved in). The easiest way to avoid wage and social security garnishment? Resolve your SBA loan default while it’s with the bank or SBA. The SBA Offer In Compromise is there specifically for this reason: to settle the debt for a reasonable sum so you can move on with life.

Is there a light at the end of the tunnel?

Well, there certainly can. But you play need to play your cards right. The process of getting your SBA OIC approved usually doesn’t fall into place by accident. Here are some “dos” and “don’ts” that I preach to anyone who will listen:

Don’t Avoid Your Lender

It’s certainly traumatic to go through a business failure. But when you bank comes calling, you need to be responsive. If you avoid dealing with them, they’ll assume you have walked away. When that happens, they will either sue you, or close their files and refer it to the SBA. If you ignore the SBA, the file go to the treasury, where SBA loans go to die.

I get calls every few months from people who got the SBA 60-day letter.

“Sure, I can help with that, I tell them. When did you get the letter?”

“6 months ago. Is is too late?”

Yup, it’s too late. There is nothing more frustrating to me than hearing from a borrower who could have settled. All they had to do was pick up the phone and call me. I could have settled their personal guarantee for a very reasonable sum. Instead, they avoided the icky feeling of having to deal with their defaulted SBA loan as for as long as possible. Then letter from Treasury (with added 28% penalty) arrives. Of course, that grabs their attention and they begin to look for help.

I know having to explain in excruciating detail how your business failed, and how terrible your personal finances are, is not a fun experience. But do you know what’s even less fun? Having the Treasury garnish your wages, your federal tax refund, and your social security for the rest of your life.

Don’t Take On More Debt To Save Your Sinking Ship

Your business loses money each and every month. Despite your best efforts, it’s simply not profitable. Rather than face the inevitable truth, many owners turn to credit cards, their 401k, or their home equity loan. I’m not saying that your business isn’t worth fighting for. But you need to take a good hard look in the mirror. Do you honestly believe the business is salvageable? Because if it’s not, taking on more debt is not going to do anything but buy you a few more weeks or months. Eventually, the money will run out.

Don’t Hold On Too Long

You haven’t paid yourself since the doors first opened. You have to beg, borrow, and steal to make payroll every month. I get it. This is the legend of entrepreneurship. Fight, claw, and battle your way through adversity, and come out clean on the other side. But it doesn’t always work like that. Grit is good, but so is knowing when to call it quits. If you accumulate massive debt and plow all your savings into the business, it could substantially hurt your ability to successfully work out an SBA Offer In Compromise.

Don’t Put Every Last Dollar You Have Into The Business

This is cousins with “don’t hold onto your failing business for too long”. Have you heard the old adage that “you get something for nothing”? Well, it holds true for SBA loan default. If you expect your lender to potentially forgive hundreds of thousands of dollars of debt in exchange for nothing, you are mistaken. If you want to settle, you need to have something to offer. So before you take another 401k withdrawal or put another loan payment on your credit card, think about the fact that if a settlement becomes the goal, you need to have resources to draw from.

Don’t Sell The Business Assets Without Permission

One of best ways to kill your OIC before it starts is to sell the business assets without your banks permission. Sometimes it’s an honest mistake. Other times, people are trying to sneak one past their lender in order to line their own pockets. Either way, the SBA takes selling assets without the bank giving you the green light will seriously jeopardize your chances to settle.

Don’t Fraudulently Sell The Business Or Business Assets Or Mislead Your Lender

If your business is on the edge of collapse, it can be stressful. Beyond stressful, actually. And in stressful times, you may be tempted to take some bad advice. Specifically, the idea of selling your business to a friend, business associate, family member or a new entity you’ve created. The SBA is clear that misrepresentation is a no no, and if you do attempt it, it could jeopardize your OIC:

I’ve written about this before, and my bottom line is that when you mislead a lender, it’s not a strategy. It’s unethical and fraudulent. I got a call about this just the other day. A nice woman told me that she had called one of my competitors, and they pitched the idea of selling the business to a friend.

She asked if their “sophisticated” scheme was legal. Sure, they told her, you can sell your business to anyone you want. The part they left out was that the fact that banks and the SBA would not consider selling to a friend to be arms length. They also failed to mention that they would hide the fact that the whole point of the transaction would be to settle the debt (under false pretenses), then take the business back later. And I can tell you with 100% confidence that the SBA would NEVER approve an OIC if they know that was going on.

Don’t Omit Information From SBA Form 770 (SBA Personal Financial Statement for the OIC)

It can be tempting to leave that investment account off your PFS (SBA Form 770). Keep in mind that your bank has ways to catch you making an intentional omission. You submitted a PFS at loan inception, and likely sent them others as part of your required annual disclosures. If they catch you leaving major assets off your SBA Form 770, that will eliminate any goodwill that may exist between you and your lender. If you lie about this, they will wonder, what else are you lying about?

Keep in mind that being careless about the information is just as bad as omitting information. The bank and the SBA want a CLEAR picture of your personal financial situation. “Ballparking” your personal expenses, leaving your new boat out (because you’ll know how they’ll feel), and making no effort to determine the true value of your home all make it harder for the bank to do their job.

I understand that it sucks to have to pony up right after you lost your investment in your business. You’ve lost so much already. It can be tempting to “protect” what’s left of your net worth. But trust me, there are a million different ways that a bank and SBA can get information. The last thing you want is to get caught in lie while you are in the middle of OIC negotiations.

Don’t Assume Bankruptcy Is Your Only Option

When it comes to SBA loan default, there are always alternative paths to take. One path may be OIC, another may be bankruptcy. The million dollar question is which is right for you? I’m not here to tell you that an OIC is always the best option for all people. Likewise, a personal bankruptcy is not always the answer for everyone either. What I AM saying is that you should explore all your options, then make an informed decision. Nobody ever regretted understanding all their options, especially with so much money on the line.

When it comes to settling, I generally find that the more money a borrower owes to more creditors, the harder it is to get the entire situation resolved. It kind of reminds me of trying to herd cats. If you have one or two to deal with, it’s never easy, but is at least manageable. If you have 10 cats? Forget about it!

Same goes to settling with creditors. If you just have your SBA loan and a few vendors to settle with, it’s doable. If you have your SBA loan, your landlord, a business line of credit, a merchant cash advance, and 5 credit cards? It only takes one large creditor to sink the whole ship. Why settle with 6 other creditors if one that you owe $100,000 to is going to force you into BK anyway?

When you are looking at your options, it’s important to know which type of BK, if any, you will qualify for. The cost of a bankruptcy attorney for a chapter 7 vs a chapter 13 bankruptcy can be very different. How much of your debt is reduced can also be much different. If your debt is not eliminated, but merely reduced, I’d argue that in some cases it would just make as much sense to settle outside of BK. This is especially true if your creditors are willing to negotiate with you without you having to resort to the BK.

Again, I’m not saying one approach is right for everyone. There is nuance to each approach that is worth understanding. There is a lot of money at stake here, so making an informed the decision could save you hundreds of thousands of dollars.

Do Understand What You Signed Up For As A Personal Guarantor

It happens more often than you’d think. Guarantors call me protesting that their lender said they were signing for the business only. But there it is, plain as day. A personal guarantee with their name on it, that they signed. This is a general life lesson that is applicable to SBA loans as well: if you don’t understand what you are signing, get some advice from an attorney who can explain it. I understand the pressure to “just sign it” at closing, but a little embarrassment now is better than a having your bank account levied later.

Do Submit A Complete SBA Offer In Compromise Package

The urge to just “get it over with” can be tempting. Fill out some forms as quickly as possible, submit them, and cross your fingers. I understand that just thinking about the whole ordeal can make you a bit queasy. But taking that approach can not only cost you thousands upon thousands of dollars, but it can actually prolong the process. So let’s do this instead. Be thorough and meticulous. Please don’t take this to mean that you should write them a 10 page letter about your sad story. By meticulous, I mean don’t round dollar amounts to the nearest $1000, don’t fudge numbers, and ensure you have fully disclosed your personal financial details. If you show little to no effort, your lender will assume you are either not serious, or making up numbers.

Don’t Getting Aggressive With The Bank

I’ve had a few clients over the years who want me to pound on the table and get downright nasty with the bank. That’s not my style, and it’s completely ineffective. I usually find that nothing is lost in most situations by being courteous.

While I can’t say that’s the case 100% of the time for me, I do try to keep that in mind when I deal with lenders. Yes, I get frustrated. Yes, I sometimes have to deal with incompetence. But that doesn’t mean I get nasty. If your banker isn’t doing their job, we can always attempt to go over their head. If your banker gives you an answer you don’t like, again, we can appeal to management. Either way, getting aggressive will almost universally make them defensive and less likely to give you the benefit of the doubt when they are on the fence about your OIC.

Why can’t my lender just give me a break. I already lost so much!

An SBA workout officer’s jobs boils down to two major responsibilities:

#1 – Gimme The Loot

The first major responsibility is to recover as much cash as possible. There is no “compassion” component to the job. They can’t look the other way and give you a break for being a nice guy, or because you’ve already lost a ton of money following the SBA loan default. If they think you have money, and you won’t pony it up, they have no choice but to pursue it via legal channels.

The only official communication that I’ve seen that I’d considered to be compassionate is that the SBA instructs lenders to avoid foreclosure on personal residences unless all other avenues have been exhausted.

#2 – Protect the SBA Guarantee

The second responsibility of an SBA workout officer is to protect the SBA guarantee. And by “protect”, I mean that they need to service a defaulted loan in accordance with the SBA SOP (Standard Operating Procedures). Because if they don’t, the lender is a risking what’s know as a “repair”. This is when the SBA reduces the amount paid to a lender under the guarantee as a result of negligence of in adherence to SBA servicing rules. All the major lenders live in fear of repairs. And for this reason, it frequently drives the decision making in an SBA Offer In Compromise. Did you ever see those bracelets that says “What Would Jesus Do?”. Well, SBA lenders are always asking “What will the SBA do?” The last thing they want is to be told by the SBA that they did something wrong.

For example, let’s say your home has $250,000 in equity in it, is pledged as collateral, and you offer $50,000 to settle the debt. If your bank were to accept this, it’s very possible that the SBA would take issue with it, despite the fact that most lenders are able to make this decision without SBA input. The SBA could make a repair for up to $200,000 as a result of this kind of decision. This is a prime example of why your lender can’t just give you a break. Because if they do, they may be paying for it out of their own pocket.

Great, you’ve done a sufficient job of scaring me. But seriously Jason, what can you do that I can’t do myself?

Sometimes people come out and ask me this question directly, other times I can kind of tell that they are thinking it but don’t want to insult me. Either, it’s a valid question. Let me give you a couple a recent example:

I recently helped a client get a lien on his home removed. He had a business, defaulted, then filed for bankruptcy. When he first reached out to me, he forwarded me an email from his banker. The banker was asking him to complete all the paperwork for an SBA Offer In Compromise. The only problem was that an OIC was not required! Did my client know this? No, of course not. How could he? SHOULD the bank have known? Well, yes. But they didn’t.

So how did I handle it (before you read what I did, ask yourself how YOU would have handled it!)?

I sent the lender the servicing document that dictates what lenders need SBA permission for, what actions a lender needs to notify the SBA of, and what actions the SBA gives the lender the freedom to do completely on their own. Releasing a lien? The SBA doesn’t even want to know about it….the lender has 100% authority to release a lien on their own.

At first the lender, who is a really nice guy, first tried to brush me off like a fly.

Him: “Well, you know this is a SBA loan right? Their rules are different.”

Me: “Yes, I’m a former workout officer for the largest SBA lender in the US, and I’ve been a full time consulting handling nothing SBA loan defaults. The OIC is only for settling defaulted SBA loans for less than the full balance. We’re asking for the release of collateral for cash consideration. Thus, an OIC is not required in this situation.”

Him: “But your client filed for bankruptcy, so the SBA needs to sign off on this.”

Me: “I’ve done dozens of these over the years, and they’ve all involved a BK. Unless the rules have recently changed, SBA preferred lenders have the authority to release liens on their own.”

Him: “Let me look into that.”

I emailed him the servicing document, and the next day, the bank emailed me back with a counteroffer. Clearly, someone within the bank or SBA had told him that same thing that I did.

So, what did I do that you couldn’t in this example?

Mostly, I relied on my 10 years of SBA loan default experience. Had my client attempted to go it alone, he would have compiled an OIC package, which is a much different set of information that is required for a lien release. The lender would have then sent the OIC package to a general SBA mailbox, where it would have sat for several months. Eventually, someone would have looked at it, and notified the lender that an OIC was not required because the personal guarantors filed for personal bankruptcy.

But Jason, but I don’t need a lien release. I’m in default and need and SBA Offer In Compromise. Give me an example of that situation.

Ok, sure. Here’s an example of how I pulled saved a client from the hell aka the US Treasury. I had a client that came to me at the 11th hour.

The bank had given up on him, and it was all his fault. He had made all the classic mistakes following SBA loan default. He avoided them, didn’t return phone calls, did a terrible job on the paperwork, missed deadlines, and basically did everything possible to indicate to the bank that he was not serious about settling.

By the time I got involved, the bank was telling me that they washed their hands of it. And then I went to work. I committed to having a complete package to them within 1 week. We submitted a thorough package that made an offer that represented the highest and best recovery for the bank. All the t’s were crossed, and the i’s were dotted.

Then the workout officer turned it down, citing a reason that I disagreed with. He was looking at my client’s income from a past job, but would not take into consideration that he had a new, lower paying job. I asked the workout officer if we could discuss this with his manager. He told me sure, but his boss was going to tell me the same thing.

As it turned out, his boss disagreed with his assessment. The workout officer was wrong, and I knew it.

So what did I do in this example that you couldn’t?

I knew when to push back. And that’s what you learn after 10 years of doing this. Knowing what to push back on, and what’s never going to change. The difference between the two is kind of a big deal.

In the course of negotiating an SBA Offer In Compromise, there are dozens of “deal points” that need to be considered. Navigating each and every one when on your own? With no experience or understanding of SBA default protocols? It’s a tough road to hoe.

But what about just a regular, run-of-the-mill OIC?

Ok, good point. Instead of trying to give you my best song and dance, let’s do this. See how many of these questions you can answer. If you know all the answers, then you probably don’t need me (and you should also come work with me!)

- How does the SBA determine monthly income?

- In what situations will they require you to sell your home?

- How does the SBA look at 401-k contributions?

- Will they make you sell your car or your wedding ring?

- How does the SBA look at 401-k accounts?

- Is a business allowed to remain open and settle?

- Will the SBA allow 50/50 business partners to each settle just their half?

- What expenses should be excluded from the monthly expense section?

- Why does the SBA want to know what assets your spouse and dependents own over $500?

- How long will the process take?

- Do we deal directly with SBA or the bank?

- Under what circumstances will the SBA take a file back from Treasury?

- What does it mean if I get a 60 day letter directly from SBA?

- Will the SBA accept monthly payments for a settlement?

- What’s a typical settlement in terms of a percentage?

- Does the SBA have a minimum amount they’ll consider?

- Is there a formula for the SBA Offer In Compromise?

I can’t afford to pay my SBA loan payment. What should I do?

I’m going answer your question with a question. Is your inability to make your SBA loan payment due to a short term issue, or a long term issue?

For short-term issues: Let’s say your business is waiting on funds from a reliable customer, except they were hit by a hurricane and had their factory destroyed. Or perhaps you had a fire in your warehouse, and lost half of your inventory. These are legit short term issues.

If you are having trouble paying your SBA loan due to a short term issue, many banks will be willing to give you a short term deferment of 3-6 months. Typically they’ll charge you interest only on the loan. Most banks I’ve come across won’t give you a deferment with $0 in payments, but it’s not unheard of.

Keep in mind that if you take a 6 month deferment, your payment will go up after the deferment. The reason is pretty straight forward. Suppose you owe your SBA lender $100K and there are 50 months left on the loan, that would be $2000 of principal per month. If you don’t pay principal on your SBA loan for 6 months, now you’d have to repay that $100K over 45 months, which would mean you’d have to pay $2,222 in principal per month.

If you are experiencing short term cash flow issues, the best thing to do is contact the bank as soon as you know that you’ll have trouble making the SBA loan payment. Get out ahead of it if you can’t afford to pay your SBA loan. Contact your SBA lender, and explain the situation to them. If it’s a legitimate issue that’s anomalous or short-term in nature, many lenders will work with you to get over that kind of temporary speed bump.

For long-term issues:

If you can’t afford your SBA loan payment because of a permanent change to the business, a short-term deferment won’t do you much good. If your revenue dropped by 40% because you lost a key customer, 6 months of interest will only delay the inevitable.

10 years ago, when the economy was in shambles, SBA loan modifications were given out like candy. Today? As far as I can tell….not so much. These days, the vast majority of calls I get are from people who have closed their business and want to submit an OIC. I get very few calls from people wanting an SBA loan modification.

Assuming your bank will entertain a loan modification, that would entail extending the loan maturity. Most 7a loans have 10 year terms, and banks can stretch them out to 25 years.

Realistically, if your business is having long-term issues, and a loan modification is either not available (because the bank says no), or won’t help enough (i.e. you can’t even afford the interest), you should really be thinking about closing the business.

I get it. It’s hard to think about closing the business, losing your investment, defaulting on your SBA loan, and being left with a mountain of debt. But the reality is that if the business is losing money month after month, it will actually be cheaper for you to close the doors.

Furthermore, funding those losses is going to eventually deplete your personal assets. Do you know what’s worse than losing your business and all your personal assets? Knowing that if you would have closed the business sooner, those assets could have at least gone towards an SBA loan settlement. But if you put every last penny you into keeping the business afloat, you’ll be left with nothing AND have no way to settle.

Distressed Loan Advisors (www.JasonTees.com) offer expert advice regarding SBA default and SBA Offer In Compromise, and can be reached at . or .. Live chat with Jason during business hours right on our site!