Hey there! My name is Jason Milleisen. I am the founder of Distressed Loan Advisors. I’ve been helping people with SBA loan related issues since 2009. If you would like to book a 30 minute case evaluation, you can book it HERE.

I’ve got almost a hundred YouTube videos mostly about EIDL loans HERE. I’ve also got several hundred articles about SBA loans, including some about EIDL, and every other type of SBA default offer in compromise and forgiveness topic you can think of.

Today, I would like to talk to you about your EIDL loan collateral. I do get a lot of calls from people whose businesses have closed and they wanna sell the stuff and they’re not quite understanding, what they signed up for as for a what they can and cannot do with business assets that have been pledged as collateral. So, I thought it would be helpful to go over that.

The most common thing that I see is people just want to sell all of the assets and don’t realize that it does require SBA approval. So in other words, if your business closes and the sale of the business assets is not gonna be going to be enough to pay off your loan in full, you need to get the SBA’s permission in writing to sell the stuff.

So, if you owe them a $100,000, and you’ve got $5,000 worth of inventory, you can’t just sell that stuff without first getting their permission. It’s known as a fraudulent conveyance and you can’t do it.

In reality, I think the likelihood of something terrible happening is not high, but at the same time, it’s not zero. So, if the SBA ever sort of, um, you know, became competent, they could come after you if you sell assets without permission.

More to the point they could come after, the collateral. So, if you sell it to Joe Schmo, can you imagine that guy’s reaction when the SBA comes calling for the equipment that you sold without their permission?

Bottom line is this: don’t sell the stuff (unless you’re paying it off) without the SBA’s permission.

But that’s not actually the main point that I want to talk about today. The main point that I want to talk about is a little bit more nuanced, but it has come up before with borrowers that I’ve spoken to.

I’ve had people come to me and say, :I understand I can’t sell the collateral that I had when I took the loan, but I’ve acquired other stuff since I took the loan. So that’s not pledged as collateral, that’s separate.”

And the answer to that is, “unfortunately, you are incorrect.”

The EIDL loan documents (security agreement) are very clear about this. The collateral that you pledged includes all business assets owned between the time that you sign it and the time that you pay it off. Anything that’s not specifically pledged to someone else, is pledged as collateral.

So in other words, if you finance a piece of equipment, let’s say you have an office and you finance a a copier machine, and then your business closes, the, the lender that financed that copy machine is entitled to that. The SBA doesn’t get dibs on that.

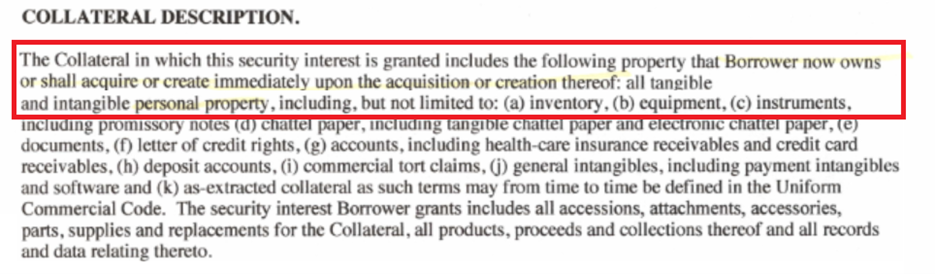

OK, here’s the nuance. The loan documents are very clear that it’s not just the assets that you owned at the time you signed the documents, it’s also the assets that you acquire thereafter.

Here is the language from a an actual EIDL security am agreement:

And so the only exception to this would be if you were able to sell the equipment, and do like a partial liquidation of the assets that is sufficient to pay off the SBA, then it doesn’t really matter.

But if you plan on, selling the equipment without paying off the loan in full, even stuff that you acquired after you sign the loan documents, cannot be sold with, without the SBAs permission. because as you’ve seen, the SBA says now or acquired in the future.

So people who come to me and say, “oh, I bought this after the fact so I’m good, I can sell that.” and they’re always shocked and taken aback.

So I’m officially putting you on notice. I’ve shown you in black and white, any equipment that is not financed through some other third party, that you acquire once you sign the loan documents does become collateral for the SBA.

Therefore, you can’t, even if I buy a piece of equipment today, a year after I took my loan, I technically cannot sell it tomorrow without SBA permission because it automatically goes into the collateral pool.

So I hope that makes sense. If you have questions, like I said at the beginning, I do offer 30 minute case evaluations.

Thanks for checking in. I’ll see you on the next one!