It’s hard to fathom, but some lenders are unclear on how to properly handle SBA loan default situations. Every so often, I come across a lender who needs me to explain the SBA protocol to them. That’s right. The very institution who holds your fate in their hands doesn’t know the rules! In the article below, I list the most common instances, and how to best deal with them.

Common Points Of Confusion

Here are the greatest hits of SBA lender confusion:

1) Authority To Release A Lien Resulting From An SBA Loan

One of the services that I offer is assisting with lien release negotiations. This is generally a release of the lien on the personal residence of an SBA loan guarantor following SBA loan default. In most cases, it’s following a bankruptcy. Releasing a lien should be pretty straight forward, as it requires less paperwork and layers of decision making. For the record, the SBA is clear that when it comes to releasing collateral, preferred lenders are not required to get SBA approval. In fact, the SBA doesn’t even want to be notified. There is an entire document that governs what action lenders need approval for, and what actions they don’t.

Yet, on more than one occasion, I’ve had lenders tell me that because it’s an SBA loan, it does require SBA approval.

2) When An Offer In Compromise Is Required

This is the cousin of “authority to release a lien”. A few weeks back, I had a potential client contact me about helping him with an SBA Offer In Compromise. This is par for the course, as the SBA OIC negotiations make up the lion’s share of my work. What was NOT normal was that this particular situation because he and his wife had already been discharged from chapter 7 personal bankruptcy.

This lender was unaware that an Offer In Compromise is reserved for situations when a borrower or guarantor is seeking to settle the SBA loan for the less than the full balance. When it comes to a lien release, there is no request for debt forgiveness. Rather it’s proposing that the lender release the lien in exchange for a cash payment.

3) Exceptions To The Liquidation Requirement

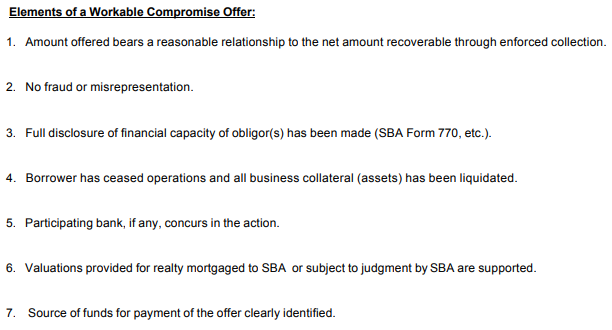

The SBA Form 1150 has a section on page 2 that outlines what the SBA refers to as “elements of a workable compromise offer”:

I call your attention to bullet point #4. This is the most common element that I site to my clients. Everyone wants to negotiate before the business closes, and I point to #4.

Borrower’s Don’t Always Know This Part, But That Makes Sense

Borrowers also often want to use liquidation of the business collateral as a bargaining chip. When they find a buyer for their business or equipment, they believe that the bank and SBA would surely be willing to commit to a settlement amount BEFORE they sale is complete. The thinking is that if they (the borrower) refuses to close on the sale, the SBA will cave and commit to a settlement amount. Unfortunately, this line of thinking is wrong. The SBA will simply not do it.

Step 1: Cease operations and liquidate. Step 2: Submit OIC. In that order.

Confusion about element #4 makes sense when it comes to borrowers. This stuff has nuance and can be confusing. But for a lender?

Knowing the SBA SOP is their job, so there is really no excuse.

Nonetheless, I’ve have bankers tell me that in order to consider an OIC, the guarantor must also sell their personal residence. Obviously, this really freaks out the borrower, with good reason. It’s traumatic enough to lose your business and life’s savings, but to be threatened with having to sell your home is simply adding unneeded insult to injury.

Whenever a bank tells me something like this, I always point to #4 on the list of workable elements. Beyond that, the SBA liquidation SOP is clear that the SBA doesn’t want to displace people from their homes. They stress that banks should do their best to reach reasonable terms for a release. NOWHERE does it state that if there is an SBA loan default, the personal residence of the obligor needs to be sold.

4) What Happens After The Bank Closes Its File

I actually can’t blame the lender for this one, as I actually had very little knowledge myself of what happened to SBA loans once I wrapped up a file. We told people that it “went to Treasury”, but didn’t know much beyond that.

Now when I hear that, I get a little agitated. Banker’s have nonchalantly told me they have declined a client’s offer, but “don’t worry, they can still try to settle with Treasury”. That’s typically when I clear my throat and perform my monologue entitled “the Treasury is where SBA loans go to die”.

Wrap-Up Reports

For the record, a wrap-up is a report that lenders are required to complete once they’ve exhausted all collection options. Since the SBA is the one taking the brunt of the loss (usually around 75%), they want the opportunity to collect some of that money on their own. In the wrap-up report, the lender details what happened up to that point, including why they believe that further collection action would be unfruitful.

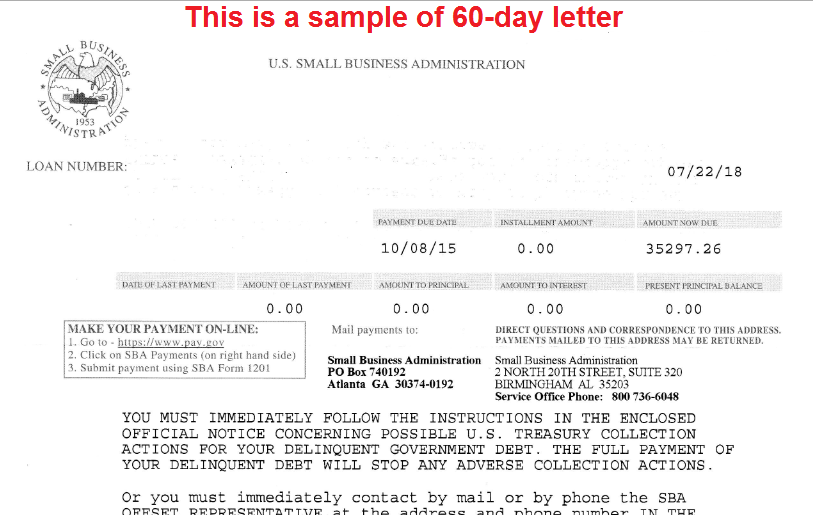

60-Day Letter

I’ve written extensively about 60-day letters here and here. The 60 day letter is the proverbial “last stop on the train”. This is the final attempt to work out a settlement or repayment plan. After that, the SBA refers the file to the Treasury. Helpful tidbits:

- Not every 60-day letter comes from the same SBA office. It depends on your locations and the loan type.

- If you wait until day 60 to contact them, the file will likely be referred to Treasury. Once it’s at Treasury, your pleas to be returned to SBA are likely going to fall on deaf ears.

- The 60-day letter from SBA is your last chance to work out a reasonable settlement. Once it goes to Treasury, it will be highly unlikely that you’ll get a better settlement deal than with the SBA.

Final Stop – The Treasury

In case you’re new here, I’m pretty pessimistic about how things are going to play out once a file makes it to the Treasury, and with good reason. They hit you with a 28% penalty, then act like they are doing you a favor when they offer to “settle” for 70-80% of the loan balance.

In cased you missed that math trick, they add a 28% penalty, then won’t settle for less than 70-80% of the NEW amount. So if I owe $100,000 to my bank, the Treasury will send me a bill for $128,000. If I was to settle, they’ll probably take somewhere in the realm of $90K-$100k to settle. So….not really much of a settlement. Your tax dollars at work…

Ok, so what should I do if my banker is wrong about something?

Point To The Written Facts

The best thing you can do is point to written evidence that supports your claim. Element #4 of the SBA Form 1150 is a perfect example. If a banker says you need to sell your home, point the SBA’s own document that specifically states “business assets” need to be sold.

Be Respectful

The key is to be respectful about your disagreement. Trying to bully your way into a “yes” is a tough road to hoe. So is trying to embarrass them, or go over their head to the SBA. I often state that while I certainly am not there to do their job, my past experience with this particular issue is not in line with what they are telling me. Even if I don’t convince them on the spot, it may at least prompt them to ask either a bank colleague or the SBA.

Now, if your bank is dead wrong about a topic, and refuses to bend, that may call for more drastic measures. First, you can try to go to SBA. But be warned, the SBA really wants servicing issues to stay with the lender. However, if you can point out the error, SBA may be willing to step in to set the lender straight. Keep in mind this is for blatant misunderstandings on the fundamentals of SBA offer-in-compromise. It’s not simply because the lender didn’t accept a low-ball offer.

And As A Last Resort…

As an absolute last resort, you can also contact your local representative in Congress. They usually won’t take a side, but they can make an inquiry to the SBA. The SBA will, in turn, reach out to the lender to find out their side of the story. If in the course of that inquiry, if SBA sees that your lender is bungling the process, they will likely correct the lender as appropriate.

Looking for answers to all your SBA questions in one place? Check out my Definitive Guide To SBA Offer In Compromise.