Okay guys, we’re now into February of 2023 and these days the hot topic is EIDL deferments. Click here to see all my EIDL resources.

In case you hadn’t heard the news, the SBA is not currently considering offer in compromise, so the best you can hope for in terms of assistance is getting a reduced payment for a period of 6 months.

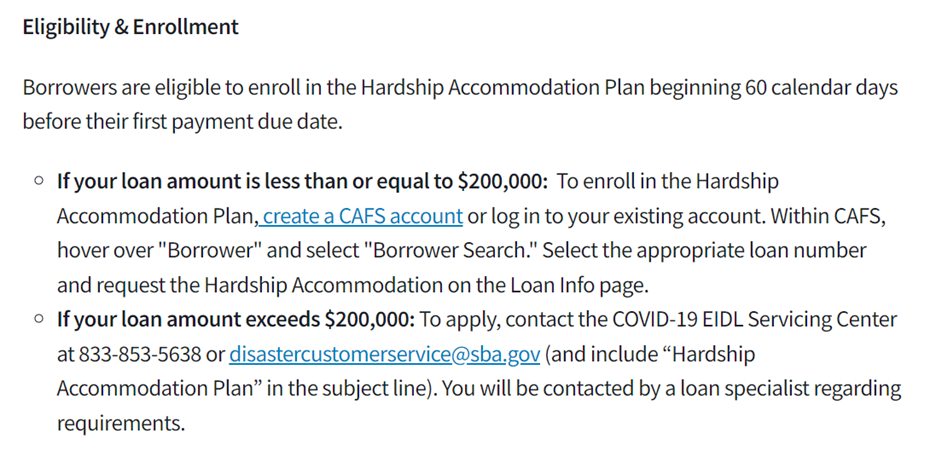

Here’s a screenshot that explains how to apply for an EIDL loan deferment from the SBA:

I hang out on internet message boards trying to keep my finger on the pulse of what’s going on, and so I get to see a lot of people talking about their experiences.

The one thing that I’ve seen is a lot of people are being declined for these accommodations. Of course I don’t know the specific details behind any of them, but I have a hunch as to why.

Back when I was a workout officer for the largest SBA lender in the country, modifications and deferments were part of my day-to-day job. Borrowers would come to us and tell us that they needed a reduced payment for a certain period of time, and it was my job to evaluate it, analyze it, write it up, and then present it to “the powers that be”.

Sometimes management would approve the deferments or the modifications, other times they would not.

So what’s the difference between an approval and a decline?

Before I tell you what they want to see, let me tell you what they don’t want to see.

Please, for the love of all that is holy, do not tell them your tale of whoa. Nobody at the SBA wants to read your view of how the government screwed their business by shutting down the economy, and then force them to take the loan because they had no other option. That will get you absolutely nowhere. (Note: I understand your frustration, but there is a time and place to vent.)

Along similar lines, telling them that the economy is bad, your dog ran away, and you’ve got this scratch in your back that you just can’t reach isn’t going to get you anywhere. This should not be an exercise and trying to make them feel bad for you. They are doing their job, and sympathy isn’t in their job description.

So what’s going to give you a better chance to get your deferment approved? It’s pretty straightforward actually.

You need to convince the reader of your deferment application that the 6 months will actually make a difference. In other words you can’t afford the payment today, but once (insert event here) happens you will be able to return to the regular payment without a problem.

For example let’s say your payment was $1,000 a month today and that you’re going to apply for a deferment so that your payment is $100 per month, for 6 months.

If you explain to them that you’ve got a lawsuit going on that’s costing you $1,000 a month, but it will be rectified by the end of July, That’s a reasonable explanation as to why you can’t afford the payment today, but will be able to afford it down the road.

If you go to them with hat in hand and say “we haven’t made any money in the last 3 years and we don’t expect to make money anytime soon”, why on God’s green earth would they kick the can down the road for another 6 months? It’s possible that they might, but then again they might also say your business is no longer viable, and another 6 months isn’t going to make a difference.

On the flip side of that coin, if your business actually can afford the regular payment and it’s clear that you can through your financials, the SBA may not see your situation is one that necessarily qualifies for a hardship accommodation.

Do you see where I’m going here? You need to hit that sweet spot of in between “I can’t pay it all and never will be able to” and “I have plenty of money”. Think of it like the three bears. You can’t have too little and you can’t have too much.

Another tip that I would say is that in these cases less words are better, and try to stick to the facts. Everyone’s had difficulties, so trying to appeal to their sympathies is unlikely to get you anything. If anything, it will distract from the overall picture that you’re trying to paint and muddy the water.

In my experience as a workout officer in reviewing these things, we’ve heard lots of explanations as to how businesses are going to get turned around. Some are good, and some are not so good. If you tell me your business has been struggling for 3 years but you’re going to invest in some marketing and that in 6 months it’ll pay off, I’m going to be skeptical.

If you tell me you’re going to bring an investor in who’s going to pump a whole bunch of money into your business but it’s going to take 6 months to iron out, I’m more likely to consider the deferment in hopes of letting you hold on long enough to pay off the EIDL loan.

Now, I want you to take this all with a grain of salt. Like I tell my regular SBA loan clients, I can’t make any guarantees with this stuff. All I can tell you is what my frame of mind was when I was reviewing these as a banking professional.

In summary, you want to keep it brief, don’t tell a tale of well, and give them a legitimate reason why you’ll be able to resume regular payment 6 months from now but you can’t afford it today.

Good luck! If you need more help, feel free to schedule a one-on-one case evaluation or check out my 90-minute audio course.