Before we get started, if you need help with an EIDL Offer in Compromise, want a 1-on-1 Case Evaluation, or want to check out my free or premium EIDL audio courses, check out my services and fees here. If you prefer videos, check out my EIDL default and forgiveness tip on my free Youtube Channel.

Hey everyone, it’s been a while since my last blog post, so I thought it’s time to provide an update on EIDL loan forgiveness, settlement, and offer in compromise as of May 2023.

Before I dive into the updates, let me offer some background for those who may not be familiar with it. EIDL loans were offered during the COVID-19 pandemic to assist struggling businesses that were either ineligible for PPP funds or had exhausted their PPP funding.

While the SBA had good intentions, they ended up lending significant amounts of money to numerous small businesses that were unable to repay these EIDL loans. Each week, I evaluate between 10 and 20 cases for EIDL borrowers, many of whom have two primary complaints about the EIDL program.

Firstly, many argue that they should not have been eligible for the loan amounts they were awarded under the EIDL program. The SBA had minimal underwriting, which led to approval for businesses that clearly couldn’t repay these loans.

While I believe in personal responsibility, I understand that these EIDL loans were granted when businesses were desperate and had limited options. It’s akin to having your head held underwater and someone offering you oxygen. In that moment, you either accept the help on whatever terms are given or face certain death.

Due to the optimism of many entrepreneurs, they chose to accept the money, hoping that their businesses would recover after the pandemic. While it worked out well for some, many small businesses didn’t experience the desired recovery. Consequently, they found themselves burdened with a 30-year loan they have little or no hope of repaying.

The second major complaint I often hear concerns interest accrual. When the SBA issued these loans, there was an automatic 24-month deferment period. However, this deferment only meant no payments were due, not that interest stopped accruing.

While one could argue that people should have read the loan documents more carefully, it’s important to consider that individuals were in dire situations and willing to sign anything to obtain the funds. As a result, borrowers will be making payments on these loans for years without seeing any reduction in the principal balance, which can be disheartening for struggling businesses.

One notable feature of EIDL loans was that loans of $200,000 or less didn’t require personal guarantees. This meant that if you borrowed less than $200,000 and had a legal entity, you wouldn’t be personally responsible for the debt. Sole proprietors without a legal entity were an exception to this rule, since they would be the borrower, and therefore, personally liable.

Although the lack of personal guarantees is helpful, it doesn’t resolve all issues. There are various nuances to consider, and I’ve been conducting numerous one-on-one case evaluations to guide people on the necessary steps to avoid major drawbacks when dealing with non-guaranteed EIDL loans. It’s crucial to remember that even without personal guarantees, there may be potential tax implications that need to be understood and addressed. (This one tidbit will cover the cost of a case evaluation many times over).

For a long time, the SBA was unwilling to consider any form of settlement or partial forgiveness for EIDL loans. This lack of responsiveness, along with slow response times, has frustrated many individuals. Personally, it took several weeks and follow-ups before I received a response from the SBA, and even then, it was often an automated or boilerplate reply.

Finally, in April 2023, the SBA responded and provided me with the application for offer in compromise specifically for EIDL loans. Since then, I’ve been discussing the option of offer in compromise with dozens of EIDL borrowers and determining whether it would be suitable for their situations.

To clarify, an offer in compromise doesn’t make sense for every borrower due to a few key reasons.

Firstly, it is generally required that the business be closed for the SBA to consider negotiating a settlement. I have been approached by several businesses asking if they can pursue a settlement while still operating, but historically, the SBA has not been agreeable to this.

However, considering the unique nature of EIDLs, I reached out to the SBA directly for clarification on this matter. Unfortunately, I am yet to receive a response, but I will update if I hear anything contrary to the belief that the business needs to be closed.

Another reason why the SBA’s offer in compromise may not be available to everyone is that it necessitates demonstrating financial hardship and an inability to pay. In simple terms, if you have the means to repay the loan, the SBA will not be inclined to settle with you.

For any level of forgiveness on your EIDL loan, the SBA requires comprehensive financial disclosure, including a personal guarantee, personal financial statement, tax returns, and bank statements. If, for instance, you owe $50,000 but have $100,000 sitting in the bank, your chances of reaching a settlement are slim to none, and as the saying goes, slim just left town.

Currently, I have already submitted one offer and am working on several others. While we await a decision, there are a few important details to note for those interested in pursuing an EIDL offer in compromise.

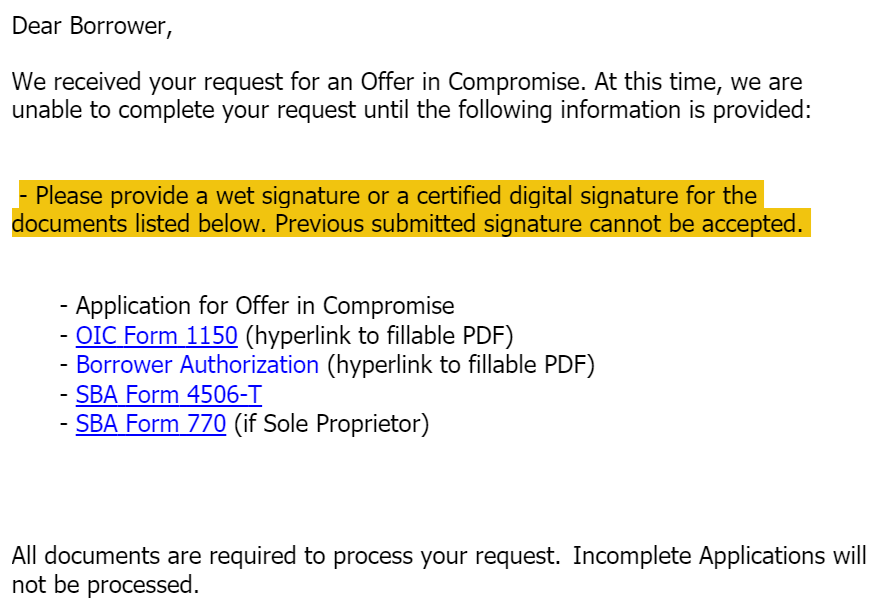

Firstly, the SBA has become more particular about how documents are signed. It seems rather unnecessary to me, considering we have been following the same signing process since I began this work in 2009. However, they are now placing greater emphasis on minor issues, such as whether you provide a wet signature (physically signing the document and then scanning it) or if you type your name on the signature line.

Although I don’t consider this to be a significant obstacle, we will comply with their requirements despite the apparent triviality.

The second issue we encountered was when the SBA requested optional information that they claimed was missing. It appears they were unable to determine this on their own, leading them to email my client and inform her that the package was “incomplete”. Clearly, someone hired to be a box checked was unable to figure out on their own that some boxes weren’t required to be checked.

Fortunately, resolving this was a simple matter of emailing them back and explaining that those items were not applicable. However, one would expect the individuals reviewing settlement offers to possess enough understanding to realize this.

These minor issues, however, pale in comparison to the bigger picture. I am hopeful that these will be the last minor obstacles we encounter. If most of our offers in compromise are approved, then the aforementioned inconveniences will have been worthwhile.

Many people have been asking me about the terms on which the SBA is willing to settle. Until I have a track record specifically with EIDL loans, all I can provide are generalities.

In other words, I have an understanding of what the SBA has looked for in other types of regular SBA loans and disaster loans in the past. However, given the unique circumstances surrounding EIDL loans, I wouldn’t be surprised if the decision parameters differ slightly from what we have seen before.

Only time will tell, but I will provide updates as I gather more information. You can check back on this blog or visit my YouTube channel for the latest updates. As always, I’m available to 1-on-1 case evaluations, which can be booked here.

Jason Milleisen is the founder of Distressed Loan Advisors. Since 2009, Jason has counseled thousands of struggling SBA borrowers, and settled hundreds of SBA loans, resulting in over $50 Million in SBA loan forgiveness.