Don’t feel like reading? This article is also in Podcast form:

Hi there! My name is Jason Milleisen, founder of Distressed Loan Advisors. I hope this article helps you with whatever SBA troubles you’re having. I know that sometimes you really just need to speak with someone, in which case you can schedule a case evaluation with me. Now, on to the article…

When is comes to settling SBA debt, borrowers often panic after they default, and attempt to rush through the OIC process. Just yesterday, my client told the bank (without checking with me first) that he would send the OIC (SBA Form 1150) form to them with a days notice. I don’t have any of his financials yet, so how can we draft an offer!?

Folks, this is not the time to rush through the process. This is the time to be meticulous. Cross every t, dot every i. With that in mind, here is my list of things you want to do, and things you should avoid doing.

Be An Open Book

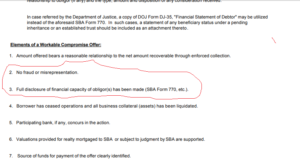

Any settlement discussion is predicated upon good faith and full disclosure. And don’t just take it from me. Look at page 2 of SBA Form 1150. If it’s too hard to see in the screenshot, you can look at elements 2 and 3 here.

It may be tempting to leave off your retirement account, kids college funds, or that investment property that has tons of equity in it. The problem with leaving stuff off is that if the bank finds out, it’s going to hurt your chances of settling.

But how would the bank know if you left asset off your PFS? A few ways, actually.

The easiest way for them to check is to review past Personal Financial Statements that you submitted. They are always required when you apply for a loan, and in many cases, an updated PFS is required on an annual basis.

If the bank obtains a judgement against you after you default, they may send you an information subpoena. The Information Subpoena is a legal document signed by the Court Clerk that orders the Debtor or others to answer questions about where the Debtor’s assets are located. If you answer untruthfully or don’t respond, it could result in an arrest.

Public record searches can also reveal real estate that is in your name. When I was a workout officer, I’d check the local county clerks site if I thought a borrower was holding out. Finding a property with equity could mean paying off the loan in full – not settlement required.

Be Thorough and Stay Focused

I’ve preached this in about 9 different articles, but it’s important. So I’ll mention it again. Treat the OIC with the same level of concern that you treated the loan application.

I’ve had too many people come to me AFTER their first OIC was rejected, and show me a car wreck of an OIC package. Missing information. Hastily written offer. Long sob stories that have no bearing on the decision.

Settlement offers that are missing information are likely to be rejected or kicked back to you. If it technically has all the right info, but just poorly executed or hard to follow, it’ll be rejected and you may have no idea why.

Whenever I assemble an OIC package for the client, I always have a checklist. And I always stick to the facts. I’ll put a line or two about a sob story if my client absolutely insists on it, but the main narrative should always focus on the numbers. WHY you don’t necessarily have the money doesn’t really matter. They key is to outline what you do have, it’s not sufficient to pay in full, and why you can’t raise more.

Keep Your Promises

This is a particular touchy subject for me. The borrowers who casually make promises to their bank, then break them, also tend to do that to me.

“I’ll get you that paperwork tomorrow” they say. Then a week later, I’m following up, reminding them that we told the bank we’d have it to them already.

“I should be able to pay you next week” they tell me. A week later, no payment.

I have two theories about borrowers who can’t seem to honor their word:

- They have been struggling to keep their head above water for so long, they don’t think twice about telling someone what they want to hear in order to stall for more time. If it buys them a few more days, they’ll lie and worry about the consequences later.

- The borrower simply doesn’t understand the concept of under-promising and over-delivering. If you think you can get it done by Monday, promise it by Thursday. That way when you deliver on Wednesday, it’s actually early!

Be Patient and Wait Your Turn

From the time you submit your OIC package to the time it’s done, you can expect it to take 4 to 8 months. That’s what I tell all my clients.

Unless there is something majorly awry, you are best served by being patient. There is a process, and it always goes better if you let the process play out. There’s a fine line between being on top of things, and being a pain your lender’s butt.

I reserve going to the SBA for very specific circumstances, like if the bank won’t respond, or they are blatantly wrong about the OIC protocols.

Don’t be a hysterical pain in the butt. Look, I understand that this period is stressful and you want it to end as quickly as possible, but you have to understand that you are likely one of many files that are sitting on your workout officer’s desk.

What this means is that there’s going to be a lengthy process – you will have to be patient and work your way through one inch at a time. Asking your loan officer about the status every day, or every couple of hours is not going to expedite anything.

If anything, it’s going to exhaust any Goodwill that you had. I can tell you that as a workout officer, I was very annoyed with people who were constantly following up to ask for a status.

As I mentioned earlier in this article, it’s totally fine to follow up every couple of weeks. What’s not fine is to call their phone incessantly. If they don’t pick up, the reason they’re not picking up is that their phone is ringing all day long.

If they picked up every phone call, they likely couldn’t do any other part of their job. I can understand that the process can feel frustratingly slow, but as long as your bank is continuing to communicate with you and telling you that it’s in the queue, there’s no point in trying to go over your workout officer’s head.

Going to their boss is only going to confirm that you’re being aggressive. And then the boss and the workout officer will both be in agreement that you’re a pain in the butt to deal with. You don’t want to have that status at any bank.

I’m not saying you should do nothing. Stay in regular contact (checking in every 2 weeks is reasonable), and be responsive when you hear from them. But when the bank says check back in two weeks, don’t make a federal case out of it.

In theory, any OIC can be reviewed in about 10 minutes. In reality, you are one of many files on a SBA workout officers desk, and reviewing OICs is only one part of their job.

So take a deep breath. It’s gonna take a while.

Understand What The SBA Settlement Parameters Are

Imagine trying to play basketball if you didn’t know that putting the ball through the basket is worth 2 points. Or if you didn’t know which way to run with the football? It’s hard to play the game if you don’t know the rules.

When it comes to pursuing the SBA Offer In Compromise, just like sports, you really need to understand the rules of the game if you hope to have any success.

A few times a year, I get calls from borrowers who used a local attorney with no SBA experience to pursue an OIC. It usually takes about 60 seconds for me to understand what went wrong.

Sometimes, they asked for a payment plan, but wanted the collateral released immediately upon entering into the payment plan (Tip: this won’t happen. You’ll need to make all the payments before the lender will release their lien).

Other times, they are asking for 20 year repayment terms (won’t happen). And my favorite is when they want to negotiate a settlement BEFORE the business is closed (definitely won’t happen).

If You Need Help, Find An Expert

When you renovated your kitchen, did you hire a landscaper? Of course not. Well, that’s what you are doing when you hire someone (attorney or not) who has no experience with the OIC process.

They may have some peripheral knowledge, but if they aren’t truly an expert, you are paying them to learn the SBA Offer in Compromise process. Sounds expensive and risky to me.

When you renovated your bathroom, did you read articles on the internet to become proficient. Again, probably not. Of course, you realize that no matter how much reading you do, it’s impossible to become adept at anything on your first try.

While a home renovation is hard, at least there is some room for error there. If you screw up your one and only chance to settle your SBA loan? It could cost you hundreds of thousands of dollars.

Understand When An OIC is Required, and When It’s Not

The SBA Offer-In-Compromise is required when a borrower or guarantor is seeking to have their obligation released for less than the full balance after a business has ceased operations.

Here are some examples of actions that don’t require an OIC:

- Release of a lien on collateral following a personal bankruptcy discharge.

- A repayment plan (such as a deferment or modification) that calls for payment of the debt in full.

If you have a lender who doesn’t understand when an OIC is required, they could be sending you on an unnecessary wild goose chase.

Expect Something To Go Wrong

Expect the unexpected. The bank or SBA loses the file. Your workout guy hassles you over minor things. The appraisal comes in at more than you expected. The SBA rejects your offer for a reason you don’t understand.

I never know what it’s going to be, but it’s always something. And that’s usually when I earn my money.

Every once in a while, I have an OIC that gets approved without a problem. In those cases, the headache is the customer asking for a discount on my fee because it “was not that hard” after all! In other words, there is less whining when things go wrong. Go figure!

DON’T Expect The SBA To Help With A Stubborn Bank

Any OIC that goes to the SBA for approval is supposed to by accompanied by a “thumbs up” from the bank. In other words, the SBA only wants to look at an offer if they originating bank agrees with the terms.

If you make an offer to a bank, and they say no, don’t expect the SBA to step in. If you go to the SBA hoping they will go to bat for you, don’t hold your breath. They rely on the bank to vet offers. The SBA actually PAYS banks to service SBA loans.

If a bank turns down your OIC, your best bet is to continue to work with them until you find mutually agreeable terms.

Make A Reasonable Offer

Telling the bank that you lost every penny you had is not a settlement offer. If you have nothing to offer, it’s not really a negotiation.

If you pledged your home as collateral and it has $100,000 in equity in it, offering $5000 is a waste of everyone’s time.

Keep in mind that your settlement offer should “bear a reasonable relationship to the amount recoverable through enforced collection” – that quote is straight from the SBA Form 1150 instructions. In other words, if it’s clear that the bank could collect more by suing you, it’s going to be rejected.

So, how does one ensure that the offer bears a reasonable relationship to the amount recoverable through enforced collection?

That’s what all the paperwork is for. Just like when you applied for your SBA loan, an SBA Offer in Compromise submission requires a personal financial statement, tax returns, bank statements, and pay stubs.

They ask for all this info for two main reasons:

- So they can figure out what they can take from you through “enforced collection”. This means the amount they’d expect to collect if they sued you, got a judgement and went after your personal assets. Bank account levies, wage garnishments, and in some states, judgement liens on home.

- So they can compare what they figured out in #1 to the amount you are offering to settle your SBA debt.

Enforced collection doesn’t mean the same thing in every state. The reason for this is that the different states have different laws when it comes to collecting on debt.

For example, in Texas, if a property is declared a homestead, a lender can’t take it as collateral for a loan. This is not the case is most other states.

Enforced collection efforts also vary from bank to bank. Most banks tend to focus on the big stuff: homes with equity, bank or brokerage accounts, and wages.

But every once in a while, a less experienced SBA lender (typically smaller credit unions and community banks) will go over the top. In some cases, I’d even call it spiteful.

I once had a client call me in a panic because the Sheriff was at their home saying the lender sent them to levy their personal assets. What a jerk that lender was…clearly he sat alone during lunch when he was a kid, and this was his way of feeling powerful.

I hope that these tips were helpful to you as you assess your SBA default options. If you’re interested in a case evaluation, you can schedule that here.