Hi folks! Welcome to my website. My name is Jason Milleisen, founder of Distressed Loan Advisors. I’ve been helping SBA borrowers since 2008 (SBA settlements are all that I do!). I know articles can be helpful, but nothing can replace a conversation. If you’d like to schedule a consultation, you can do so here.

Before we get too far into the weeds, I’ll cut to the chase. By far, the question I get most often about SBA Offer In Compromise in 2022 is “Is the SBA being more lenient about settlements due to COVID?”

In a word: no. In my experience, when it comes to SBA Offer In Compromise, the SBA has been treating defaulted SBA loans in the same manner they always have.

If your business has closed (this is almost always a requirement, settling SBA debt when a business is still operating is rare), the SBA will consider PARTIAL (not full!) forgiveness.

Whether or not the SBA will settle a loan for less than the full balance will, as it always has, depend on the financial wherewithal of the personal guarantors. There are no exceptions for COVID. Sympathy has never been a factor in their OIC decision process, and it doesn’t appear to be changing, even because of COVID-related business failure.

“But THEY forced my business to close for months!” is the common response I get. I get it, guys. I really do. I’m on your side. I wish my answer were different, but it’s my job to tell my clients the truth, not what they want to hear.

So here we are in 2022. We’re finally seeing the world get back to normal. The latest wave of COVID subsided, mask mandates are largely done, and most of us, life is finally (after 2+ years!) getting back to normal.

I don’t know about you guys, but by late 2020, I was sick and tired of dealing with the coronavirus pandemic. It felt like it started years ago, but in reality, at that point it had only be months since the whole world went to hell in a hand basket.

I remember at the time thinking that if the whole country was going to shut down, it was going to be catastrophic for our small businesses. I predicted that my consulting business, which of course deals with helping people through the default process, would take off like a rocket.

I turned out to be wrong – they passed the CARES act, which was intended to help businesses through a short period of financial difficulty. The idea was for the government to cover 2 months of salaries for their employees. As we all know now, two and a half months was not enough time for the virus to disappear.

The CARES act did an additional important thing for all the SBA borrowers out there. They covered SBA loans and made 6 months of payments for every single SBA borrower. They didn’t defer them. They actually paid them. The SBA actually sent money to cover those payments.

Around November 1st 2020, a lot of those SBA gifts have run out, and like clockwork, my phone and inbox had started to light up like a Christmas tree. But then the government extended their SBA payment deferments a few more times, and once again, my phone went silent.

Now that its April 2022, and those deferments are expiring, my phone has started ringing again. In particular, people are getting the SBA 60 Day Letter.

While COVID seems to have subsided, there’s still a ton of pain and carnage to be sorted out. I’m here to help you navigate SBA loan default, like I have been since 2008 . If you need help settling your debt and negotiating the release of your personal guarantee, please reach out for a case evaluation.

Now that life is getting back to normal, this is a good time to get back to the basics of SBA loan settlements, otherwise known as SBA offer in compromise.

The info below are the very foundations of what constitutes good behavior and best practices when it comes to the SBA offer in compromise.

Good Communication Is Key

If your lender is constantly chasing you, constantly asking you for information that you don’t provide, and generally feels that you’re not easy to work with, that could kill a settlement right out of the gate. I promise you, the last thing you want is for your loan to be referred to the U S treasury. They will add a 28% penalty. And I consider them to be generally unreasonable.

When it comes to settlements, it’s simply not a position you want to be in. Do yourself a favor and respond to letters, return phone calls and emails. I understand the temptation to avoid it. This whole situation is very in pleasant. I get that, but this is not the time to run and hide. You’re going to have to deal with the situation eventually. And in my experience, it’s always better to deal with it sooner than later.

Make Your Banker’s Life Easy

The easiest way to make your banker like you and create some goodwill? Give them full disclosure and make reasonable arguments. There’s nothing more frustrating to me than having a client who doesn’t understand how it hurts their chances with hastily put together paperwork with flimsy arguments that make no sense.

While I helped my clients prepare the personal financial statement, otherwise known as SBA form 770. I’m often shocked at how little effort people put into them. Of course, it’s my job to make sure that we get that information correct. But I often have to reiterate to my clients that the bank is relying on this document to make a decision. And so it’s not the sort of thing you fill out in a minute or two

Along the same lines, I’ve seen some people try to make some silly arguments to me that I tell them will not get us anywhere. Arguing that your bank got a bail out and so should you is not going to make you any friends. Arguing that it’s the government’s fault because they required shutdowns is not going to get you anywhere. You need to understand that they want their pound of flesh. It’s going to hurt to have to pay for this settlement. There are no sweetheart deals. They’re not giving anything away.

So, you have to make realistic assessments of your situation. For example, I have a client that we’re going to be submitting an offer for, and she earns a decent salary. I pointed out to her that in the state that she lives in, wage garnishment can amount to 25% of take home pay. She didn’t like that answer, but she accepted that our offer needs to be somewhere based in the reality that wage garnishment is an alternative for her lender. This is what I mean when I say you need to make reasonable arguments.

Lay Your Cards On The Table

There’s no use in trying to mislead your bank. If they’ve done a lot of these before they can smell something fishy from a mile away. If they ask for bank statements, give them bank statements. If they want to know how much money you make, be honest about it. There’s a big difference between making an argument in your favor and giving false information. What I do is not the former, and most definitely NOT the latter. My job is to take the facts and try to figure out an argument that is reasonable and supports our position that a settlement is needed. The bank is savvy enough to understand the difference between someone who needs a settlement and somebody who just doesn’t want to pay for a business that’s closed. There’s a big distinction there.

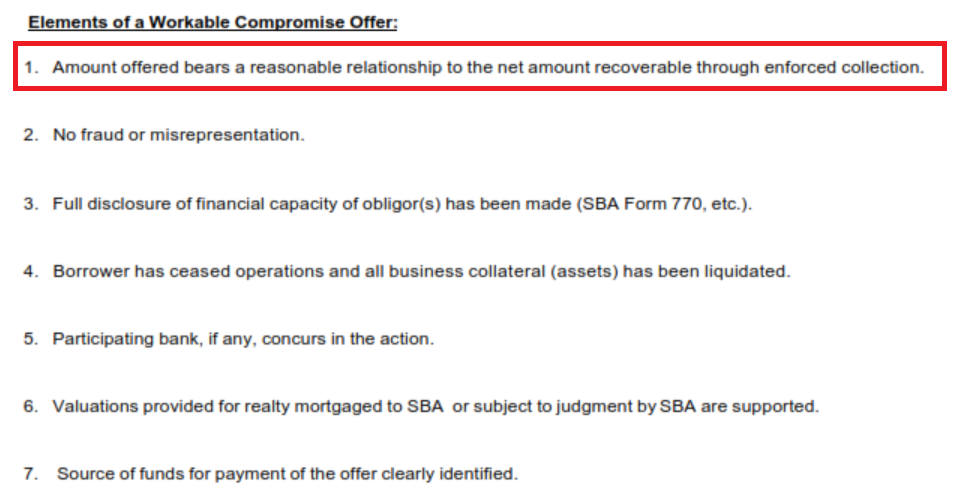

There must be a reasonable relationship between the amount that you offered and the amount that they could potentially get through what they called “enforced collection” (i.e. they sue you). The screenshot below is right from SBA Form 1150.

I alluded to this above. If they can garnish your wages and get a thousand dollars a month, they’re not going to accept you paying a hundred dollars a month. Along similar lines, if you’ve got $100,0000 sitting in the bank, they’re not going to take $5,000 to settle. The whole point here is they understand that they have options when it comes to collections. Our job is to make an offer that makes them indifferent as to whether or not they sue you, or if they just take the offer that’s on the table. This concept of a reasonable relationship is one of the main workable elements that’s listed right on SBA form 1150.

You Must Prove Financial Hardship and a Lack of Ability to Pay.

There is a distinction to be made here. Lack of ability to pay means you simply don’t have the resources. If you owe a million dollars, they may look at your situation and say, yes, we believe you can’t pay this regular monthly payment, but that may not be enough to warrant a settlement. They also want proof of financial hardship. Are you paying your other creditors? What is your credit score look like? Do you have purchases that are inconsistent with somebody who’s experiencing financial hardships, such as vacations or eating out a lot?

There is no formula that they have that will say yes, you are experiencing financial hardship or no, you’re not. But I always say that if a reasonable person looked at your lifestyle, would they be able to tell that you’re experiencing financial hardship?

There is No Set Settlement Percentage

Everyone asks me this question and I always tell them, yes, there’s a range of what people settle for, and it’s a fairly wide range. I tell them at somewhere between 10 and 40%, but then I also tell them that I don’t find those percentages to be particularly helpful in any particular case, because those numbers are essentially backed into. In other words, I don’t arbitrarily say let’s start at 10% and hope they accept it with the expectation that it might go as high as 40%. What we have to figure out is where can you get money from, and where do they expect you can get money from. Typically, what happens is the dollar amount that we can figure out falls in somewhere between 10% and 40%. That is a whole lot different than arbitrarily applying a percentage to the amount that you owed.

Home Equity is Only a Starting Point

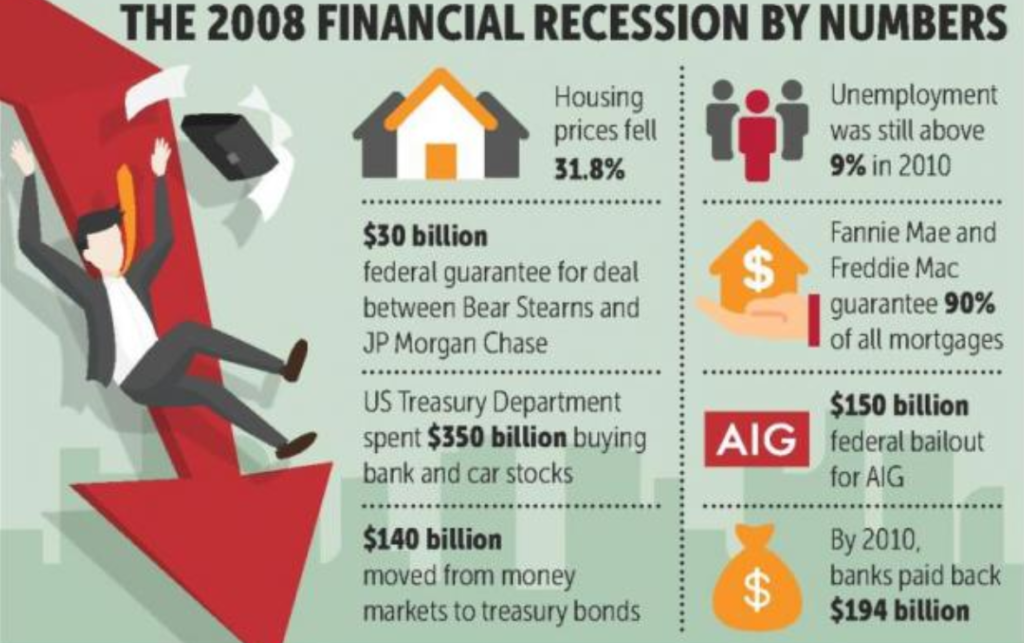

The financial downturn caused by COVID is different than in 2008 for one major reason. The reason it’s different is that because in 2008, property values tumbled as a result of the financial crisis. I specifically remember in California seeing home values fall by as much as 50%.

Contrast that with the pandemic. Many suburban areas are skyrocketing in terms of value. People are fleeing cities for the more spread out suburbs. As a result, if you pledged your home as collateral and prices have got up, that likely means that there’s going to be equity. If there’s equity, the bank is going to expect the settlement offer to reflect that.

The only way that that would change would be a financial markets melted down again to the point where mortgages were harder to get. And perhaps all of a sudden prices will begin to plummet. As of the writing of this, that is not the case in the US housing market.

You Still Owe the Money, Regardless of the SBA Guarantee

The SBA guarantee is for the lender only it does not relieve you of the obligation to pay. I’ve had people come to me and ask if they can offer the bank of their portion (typically 25%) and thereby they would be willing to settle the whole thing since the SBA, and not the bank, that would be taking the loss.

Unfortunately, this is not how it works. The SBA and the bank share losses on a pro rata basis. That means that if the SBA reimburses the bank for 75% of the loan balance, then going forward, 75% of any collections would go back to the SBA.

Also, just because the SBA reimburses the bank, it does not cancel your legal obligation to repay the debt. It does NOT mean that you as a guarantor are off the hook. All it means is that the SBA is the one who’s taking the loss instead of the bank.

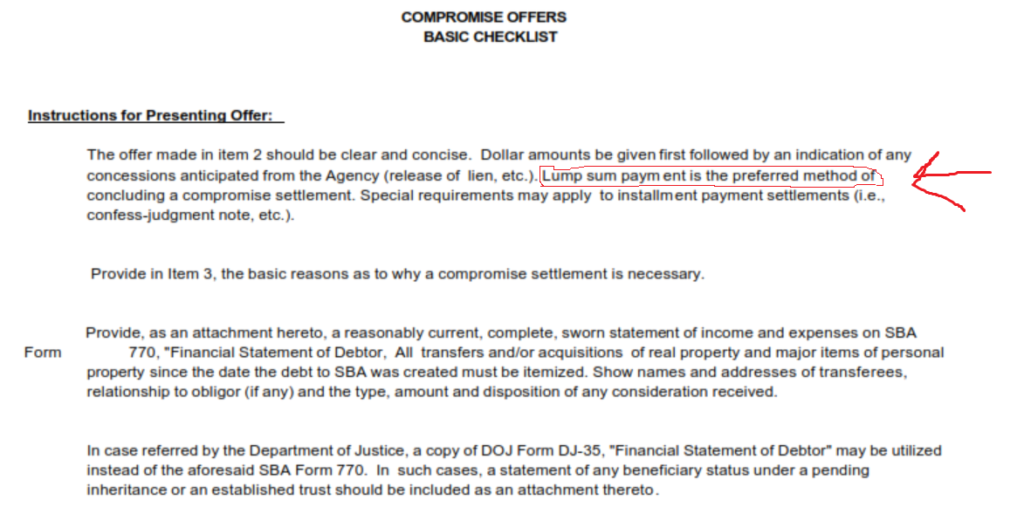

Lump sum is Preferred, but Payments may be an Option

Whether or not a lender is willing to accept payments is up to them. The SBA does have a stated preference that a lump sum is preferred, but they are willing to consider monthly payments if it can be demonstrated that a borrower doesn’t have a lump sum assets, nor do they have anywhere to borrow from.

I try to discourage monthly payments because if someone misses even just a single payment, it can invalidate a settlement. If you made 59 payments and missed the 60th payment, the bank could cancel the settlement and state that you still own the original amount while keeping what you paid up to that point. Not a great feeling if you’re the borrower.

Here’s a screenshot right from the OIC form:

Your Credit Score Matters

When you submit your OIC, they’re going to run your credit. And if you’ve been paying everybody but the SBA, they may want to know why everyone else is getting paid except them.

Along similar lines as discussed earlier in this article, they may look at that as an indication that you’re not experiencing true financial hardship. People who are experiencing financial hardship tend to miss payments on more than one obligation and not just their SBA loan.

So, in the case of an SBA Offer In Compromise, a poor credit score can actual be considered a positive.

Having More Creditors Makes it Tougher to Settle

I have people that call and they want to know if they should file for bankruptcy, or if they should try to settle. I, of course, tell them I’m not a bankruptcy attorney so I can’t give that kind of advice. But I do tell them that in general, if you’ve got five or six creditors that all need to be settled with, it’s going to make it more difficult. Especially if one of them says no, and you can’t afford to pay them, then it doesn’t make sense to settle the rest of your debt.

If you only have your SBA loan and a landlord, it makes it much more manageable to settle. I’m not saying it’s impossible to settle with multiple creditors, but it does increase the degree of difficulty. Think about it like juggling. Most people can juggle one ball two when you get to three gets a little harder. And of course beyond that four, five, six or seven could make it almost impossible for most people.

The CAIVRS List

If you default on an SBA loan, you will be put on the CAIVRS list. It will prevent you from getting government assistance going forward, including FHA loans and federally subsidized student loans. An important point to make here is that a settlement is not what put you is on the CAIVRS list. It’s the act of defaulting. So in other words, either way, you’re going to end up on that list if you don’t pay them in fall, regardless of whether you settle.

No Bankruptcy is Required

Small business owners often ask if they will be required to put your business into bankruptcy in order to settle. No, definitely not. In fact, I can count on the number of one hand over the years, the number of clients I’ve had that put their business into bankruptcy. For most small businesses, the assets consist of nothing more than some basic low-value assets, such as restaurant, equipment, tables, and chairs.

What we really care about when it comes to Offer in Compromise is your personal guarantee. And if you file for bankruptcy for your business, that has no bearing on your personal guarantee and you will still be personally liable.

There are No Guarantees of a Successful OIC

Some people come to me looking for an iron-clad guarantee that I’ll be able to get their settlement done on great terms, and I’ll tell them the same thing. If anyone out there is guaranteeing that they can settle and that they’ve never had one that didn’t, they’re complete liar. I know of at least one company who does this on a routine basis, and I consider them to be morally corrupt because I worked with them when I was a lender and know for a fact they didn’t settle.

There are so many moving parts in these processes that it’s impossible for anybody to reasonably say that they can guarantee a settlement will be successful. We have to deal with your banker. We have to deal with your bankers boss. We have to deal with the bureaucrats at the SBA. Nobody knows whose desk the OICs are going to land on. And therefore, there’s no possible way to know how it’s going to go.

Different Offices have Different Views

The SBA has many offices around the country and which office is reviewing your OIC can make all the difference. Obviously, it’s something you can’t control, but it is something we need to understand.

I’ve had some offices that refuse to take anything less than half. I’ve had some that take refused to take any less than 20%. And then there’s others who are willing to take any percentage as long as it makes sense. There’s nothing we can do about it. We can’t ask for a different office to review it as they are all directed based on the loan amount and also the SBA loan type.

So that’s it, that’s it. That’s my refresher course on SBA Offer In Compromise. Want to talk it over with me? Schedule a case evaluation here.

P.S. COVID is the worst.