Hi there, my name is Jason. I am the founder of Distressed Loan Advisors and I appreciate you taking a moment to check out my website. If you’re here, it’s because you’re likely interested in the SBA Offer in Compromise and want to understand the process better.

If you want to speak with me one-on-one, I offer 30-minute case evaluations. If you want other resources check out my “SBA Default Blog“. If you are looking for EIDL advice, I can help with that too.

Good news, I’ve been doing this for over 15 years, so I can give you a blow by blow account of what the SBA offering compromise looks like in the year 2024.

So before we get too far into it, I want to recognize that there are different types of SBA loans and as such, not each SBA loan type is going to be eligible for the SBA offer in compromise in 2024. Specifically I’m talking about EIDL loans.

For those who don’t know, these are the loans that were given out during COVID with very favorable terms. These loans were given out with a 30 year term at a fixed rate of 3.75%.

Generally speaking, these are fantastic terms unless of course you can’t afford to repay the loan, in which case the terms don’t really matter. The important point here is that as of the writing of this article, January 8th, 2024, EIDL loans are not eligible for the SBA offer in compromise.

At this point, the best that you can hope for is a hardship accommodation, which would allow you to make a payment equal to 10% of your regular monthly payment for a six month period.

As of now, the SBA is willing to approve two six month terms for most borrowers at 10%. After that, if your loan is over $200,000, they will approve a third deferment equal to 50% of your regular payment.

If you have a loan under $200,000, you can actually go right into the SBA loan portal and renew the hardship accommodation for a third time around 10%. Some people have reported that you have to increase the payment by five or $10, but practically speaking, it’s still a low number relatively close to the 10%.

The reason that the smaller loans can do this is that those are approved in the portal typically automatically. Whereas loans over $200,000 do require an SBA employee to review your documents and at this time they have all stated that 50% for a third deferment is the absolute best they can do.

So that’s the EIDL loans. If you have more questions about EIDL loans, you can actually check out all of my blog posts and 100+ Youtube Videos that pertain to EIDL.

So when I talk about SBA offer in and compromise in 2024, what I’m really referring to in this article is SBA 7A loans and to a lesser extent SBA 504 loans.

For the purpose of this discussion, I’m going to be thinking of 7A loans since they’re by far the most common SBA loan that I work on for Offer in Compromise.

So let’s get started at the very beginning. If you’ve decided that your business needs to close, then that’s the first step. If you have any inclination or desire to settle your SBA 7A loan, one of the prerequisites is that the business needs to cease operations.

Keep in mind that that could mean simply closing the business, but selling the business is acceptable as well. Once the business has stopped operating, the next step is that business assets need to be liquidated.

This can be accomplished in a number of ways and ultimately how the sale of the assets goes down isn’t super important as long as it gets done and the lender is agreeable to the methods of sale.

NOTE: This is an important point to make. Do not sell any business assets without your lender’s permission, as doing so could result in them referring you to the inspector general for fraud.

They consider it fraudulent because you have pledged the business assets to the SBA, and therefore you do not have the right to sell them without the SBA a’s permission. So I’ll repeat: the sale of any business assets require the lender to approve them.

So, make sure that you get it in writing that you are allowed to sell the assets before you liquidate anything. There are a number of ways that you can actually handle the liquidation and it’s gonna partially depend on what your lender wants.

In some cases, the borrower themselves will use their own network to sell the assets often to a competitor or something like that. Alternatively, the business owner can simply list the assets for sale on sites like Craiglist or Facebook Marketplace or anywhere else where people might buy and sell business assets that you have to offer.

If selling the asset yourself is not possible, banks will often bring in an auctioneer who can value the equipment, and if the auctioneer has a buyer, they can coordinate that. Alternatively, the auctioneer can also hold an auction. Many of them will have online auctions with large amounts of items in them and they’ll be auctioned off one at a time.

Finally, another way that you can sell the business assets would be to simply sell the business as a whole. I often tell people to price the sale at something that’s gonna make it very attractive.

Essentially, this is a fire sale. This is not really truly a going concern situation. So sellers should be willing to be flexible and compromise on the price because we don’t want this process to drag out simply because we cannot move forward with an offer in compromise until the assets have completely been liquidated.

Once the liquidation of the assets is complete, at that point we can submit an offer in compromise package to the lender. I’ll often have clients start working on that paperwork once we know that the sale of the business assets is imminent so that the day that the sale of the assets is complete that will have an offer in compromise package ready to go.

So let’s talk about what’s included in an SBA offer in Compromise package. The SBA requires some pretty standard forms and then on top of that, many lenders have their own forms or documents that they wanna see as well. For the purposes of this article, I’m gonna talk to you about what I know for sure the SBA requires.

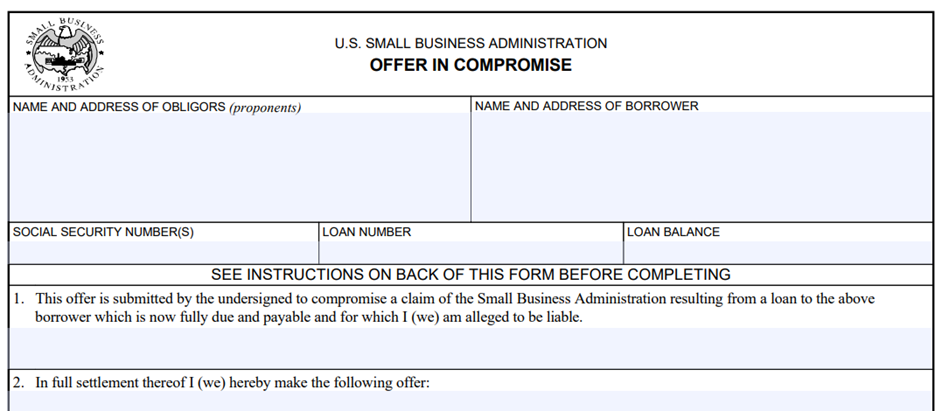

First and foremost, they’re gonna want to see two important documents. The first one is SBA form 1150. That’s the actual offer in compromise form.

In this form, you’re going to make your argument as to why the lender and SBA should approve your settlement offer. This is your opportunity to plead your case to the lender, your showing them how much you’re offer in on what terms, and using the rest of the data supplied trying to justify the amount of the offer and why it’s acceptable. It should be acceptable to the SBA and the lender.

One required thing on SBA 1150 is that you need to state not only the terms. (for example “In exchange for a payment of $50,000, I’m seeking the release of my personal guarantee and a release of a lien on my home.”)

You’re also going to need to state the source of the offer in Compromise Funds. So in other words, you’re gonna say the $50,000 will come from a home equity loan that we will obtain prior to consummation of the offer.

That’s an important point because the SBA is going to look at your personal financial statement to determine whether or not the offer makes sense and whether or not you can actually afford the offer.

The rest of the offer in Compromise Form is spent explaining your financial situation in such a way that the lender will hopefully agree that you can’t afford to pay it in full, and that the offer that you’re making is in line with your true ability to pay.

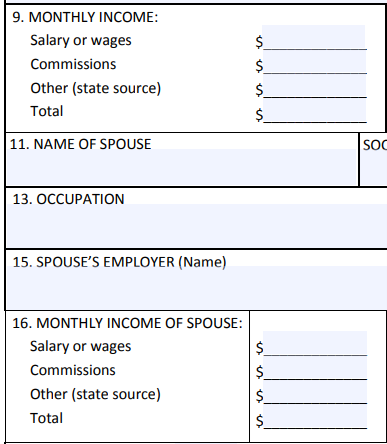

Next, you’re gonna have to do SBA Form 770, otherwise known as the personal financial statement. Keep in mind this is not the same personal financial statement that is required when you applied for the loan or even if you got a deferment.

There’s another personal financial statement, which is SBA Form 413 that some lenders mistakenly send to borrowers. Just be aware that that is not the correct form for an SBA offer an compromise and the SBA will reject it.

So as far as the SBA Form 770, this is the personal financial statement where you’re laying your cards on the table, you are showing them exactly what assets you have.

You’re showing them what your income is, and then you’re also showing them the offsetting liabilities and expenses. The goal here is to give them a real honest look at your financial statement. Like I said earlier, we’re laying our cards on the table here.

This is not the time to intentionally leave stuff off or offer some sort of misdirection in hopes that they will give you a better deal. If lenders feel that you’re not being forthcoming with them, it makes it much easier for them to decline an offer simply because they don’t trust the information.

So don’t get cute here. You want to give them full financial disclosure.

If there’s questions about how to demonstrate some of the information, because there’s nuance, you can always give them an addendum that fully explains.

Again, the goal here is full disclosure, so that anyone reading your offer and looking at your personal financial statement can fully understand your situation.

So there are a lot of sections to SBA form 770, but I’m gonna go through the major ones.

You’re gonna start by listing your monthly income. Generally I show that net of tax and then as an addendum I’ll show them the gross withholdings and then the net.

The reason I like to show the net is because you don’t want someone to do a back of the envelope calculation based on your gross and think that you can afford more than you actually can. So I always recommend showing the net.

Pay stubs are required to go along with the package and so we’re gonna make sure that the pay stubs match up with what we’re reporting on the income section.

There’s an income section both for the borrower and their spouse. Typically people do include the spouse’s income even if they’re not a guarantor, as it does give the lender an opportunity to understand the household finances.

Once we complete the income sections, we’re gonna move on to the expense section. It says fixed expenses, but I take the opportunity to include all expenses.

My goal here is for someone to be able to look at your take home income, subtract out your expenses and get a very easy estimate of what your monthly excess or deficit income is.

They’re gonna use this to determine whether or not you can afford a monthly payment. There are some things that belong on there like your mortgage payment, your utilities, or your car payment. All those items always belong there.

Then there’s other items that could be considered discretionary, which you want to be careful about. Obviously including your vacations or your boat payment doesn’t really look good if you’re trying to argue financial hardship.

And so I often will leave items like that out in recognition that hardship should not include those items. So you really want to sharpen your pencil and make sure that all of the items are, what would we call non-discretionary – you MUST to pay them and you don’t have a choice.

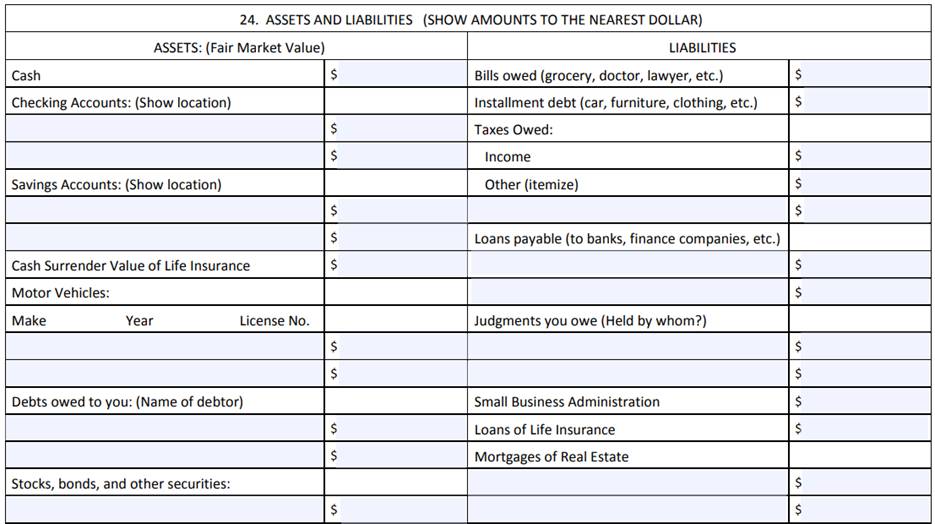

Beyond that, they want a list of your assets and your liabilities, which is pretty straightforward. I would recommend that you include all major assets including real estate, primary residence, & investment properties.

Also included are investment accounts, checking and savings accounts, and also retirement accounts. Even though retirement accounts are protected from creditors levies, it still does contribute to the overall picture.

So in other words, if you had $10 million in a 401k plan, they couldn’t actually touch that, but it’s going to impact their decision.

Along the same lines, if you have nothing in the way of savings that also paints a picture and depending on how old the borrower is, we could probably get a good estimate of whether or not what they have saved is sufficient for them to retire on.

So if somebody is 75 years old, then they have a $100K in a 401k, it’s certainly easier to argue that that person really needs those funds. Whereas if somebody’s 30 years old and has $10 million in their retirement account, it’s going to be difficult to argue that that person can’t afford to pay it in full.

Moving on, there is a debt schedule, so any loans or debts that you’ve included in your section 24 of the personal financial statement will also show up on the debt schedule.

The debt schedule is a little bit more expansive so it shows the original amount, the loan terms, the monthly payment, the collateral. Also it gives them additional insight into debts that you would’ve already listed in section 24.

There’s also a separate section for your home. It’s a little confusing, but basically there’s one section if you own it free and clear and then there’s, there’s another section if you have a mortgage.

So you’re in most cases if you have a mortgage, you’re gonna use the section 27 where it ” REAL ESTATE BEING PURCHASED ON CONTRACT OR MORTGAGE”. And so you’re gonna include all the details including what it’s worth, how much you owe, what the monthly payment is and whether you’re current.

And then beyond that they just ask some follow up questions about if you have life insurance, if you’re a beneficiary of any trusts or anything like that.

The PFS also wants to know the details if you’re involved in any litigation. So in other words, if you are suing, say you’re your franchise and stand to get some money from the lawsuit, the SBA is gonna want to know that and typically they’re gonna want a lien on those proceeds.

So that’s SBA Form 770. In addition to those two main forms, the 1150 and the seven 70, you’re going to need to include two months of all liquid assets. So that includes checking, savings, investment accounts, retirement accounts, brokerage accounts and so on.

They typically also want to see two months of pay stubs. And then there are some additional forms that allow the SBA to run your, verify your credit.

So that’s the gist of the SBA offer and Compromise forms as far as how much you need to offer – that’s really a very loaded question and honestly why people hire me.

But in general, the offer needs to be in line with your true ability to pay. The people at the SBA and the banks have seen enough of these that they’re not gonna bite on a low ball offer that has nothing to do with your personal finances.

In other words, they don’t settle for the sake of settlement. They settle when they think it’s in their best interest.

Generally speaking, the low hanging fruit as far as the SBA is concerned is equity in a home. And that’s especially true if the home is pledged as collateral. If the home is pledged as collateral, then any offer in compromise that you’re gonna make is going to have to roughly start around the amount of equity in the property. But it could go up from there depending on what the rest of your finances look like.

In addition, cash and non retirement accounts is always something that they look for. They’re not gonna take every single penny you have, but they’re gonna want a lot of it.

So if you have got money saved in a bank account or a brokerage account or some other savings vehicle, you can expect that the SBA is gonna want you to pony up a lot of that money.

Now when it comes to the SBA making a decision, what they’re really looking at is whether or not you are experiencing financial hardship and if you truly lack the ability to pay.

In addition to that, what they’re looking at is what are their alternatives here. So if you can’t come to terms with them, what do they expect that they could get if they sued you? They refer to this as “enforced collection”.

It does vary from state to state because there are different protections. So I can’t really give you a specific formula, but I can tell you that if you live in a state where homes are protected, that definitely gives you a leg up. In a state like Texas, people are never required to pledge their homes for SBA loans. And so as part of a negotiation, the SBA doesn’t have as much leverage because they can’t threaten to foreclose on your property.

But aside from Texas, if you live in a state where your home isn’t protected, the lender is going to consider the equity in your home. They’re gonna consider how much money you make and how much they could garnish and then they can consider how much money they could levy out of your accounts. Those are the major things that they’re looking for here.

If you don’t have access to any of that, the next best thing is to either borrow the money if you can qualify for a loan somewhere. But realistically, a lot of people will borrow money either from their retirement accounts or they’ll borrow money against their house or friends and family will will help them out.

I’ve had that happen on many occasions and you could almost say that borrowing from friends and family is the best place to get the money because in most cases, that clearly demonstrates that the borrower has no access to cash themselves and they actually need to rely on the generosity of friends and family.

And when the lender sees that, it makes it a much easier decision. So in other words, if a borrower doesn’t have any equity in their home, any cash savings and doesn’t make enough to make a payment, the bank & SBA are kind of at a dead end in terms of collection.

So if a friend or family member is willing to step up and fund the settlement, it generally is pretty obvious that that represents the best possible collection for the SBA.

Now I just want to talk about some generally helpful tips that would make your offer in compromise go much, much smoother.

First and foremost, you need to be proactive. The number of people that I’ve had call me over the years after they stuck their head in the sand is immense.

Here’s the thing, if the person working at the bank doesn’t hear from you, they’re under no obligation to chase you and ask you if you want to try to settle.

So if you want to try to settle, the onus is on you to reach out to them and understand what it is that they want from you in order to consider a settlement.

I always recommend asking them for their own checklist because some banks do ask for additional information above and beyond what the SBA asks for. With all that said, you need to be proactive and take this head on.

I can tell you as a former workout officer, I always looked more favorably at the files where people were fully cooperative and always communicated promptly. People who avoided me didn’t return phone calls or emails, failed to send in documentation on time or did a terrible job completing the documentation requests.

Those are loans that typically we’re gonna frown upon and likely decline. So be proactive.

The next thing that I would say is you just want to be really honest throughout the process. Lenders who do this a lot, they can sniff out BS pretty easily, and so you just want to be honest with them at this point.

They understand the business is closed and you have to do what you have to do to try to make this work. But leaving information off of your personal financial statement can only lead to bad things.

They’re likely gonna get an appraisal on your house if it’s pledged as collateral. So there’s really no point in stating that the value is much lower than it is.

Likewise, you don’t want leave off liquid asset accounts because they will often refer back to earlier personal financial statements and if they notice that you’ve left stuff off, it may be hard to get them to accept that it’s actually a mistake.

There is a section in the forms that the lender is required to fill out for the SBA that asks if the borrower has been cooperative. And while that probably won’t turn a no into a yes, it can certainly help in a situation where maybe the workout officer is on the fence.

That may turn a maybe into a yes just because you’ve been cooperative. So when it comes to selling the assets answering their questions or getting them information on a timely basis, this all contributes to whether or not the owner the bank feels that you have been cooperative.

It’s also important to remember that the SBA will not review your offer in compromise unless your lender is willing to recommend it for approval. So in other words, before the loan ever gets to the SBA, you need to get past your lender and their committee or their bosses or whoever it is that has to approve it internally.

Once your bank is willing to recommend it for approval, then and only then does it go to the SBA.

Overall, I tell people this process will take somewhere between four and eight months and it’s a very wide range because banks move at different speeds. Depending on when you submit your offer in compromise to the SBA, they may or may not be backed up with other offers. Basically, you need to hurry up and wait.

Most offers in compromise are done through the lender who forwards the package to the SBA to make the final decision. Now, in some cases, some lenders don’t want to participate in the offer in compromise process and in other cases lenders will feel that a borrower has not engaged with them and therefore they just close their file.

In these situations, the borrower will likely get what’s known as a 60 day letter from the SBA as the name implies. The borrower has 60 days from the date of that letter (note that I say date of the letter, not receipt of the letter. Sometimes people get it two weeks after the date) to work something out with the SBA. So essentially this letter is your last stop before the loan is referred to the US Treasury where it’s highly unlikely that it’ll ever settle.

Once a loan is referred to the treasury offset division, those 60 days are crucially important. I beg and plead people to get offers in as quickly as possible because you don’t do not wanna wait until day 60 because at day 60 the loan will be referred to the treasury.

Usually the SBA will look at your offer once it gets referred to the treasury and they’ll pull it back if they’re willing to approve it. But if they decline it, you’ll have no future opportunities to submit offers.

So I always recommend that you submit the offer sooner than later because if the SBA declines it inside of the 60 day mark, you could actually have a second opportunity to submit an offer with a revised or better offer.

Once a file gets referred and gets a 60 day letter, this is indicative that the loan has been charged off. Practically speaking, what that means for you is that they won’t be interested in a settlement that includes monthly payments. They’ll only be interested in settlements for lump sums of cash.

If you wanna make monthly payments to them, they’re gonna require you to pay it in full. Note that this is different than settlements through an SBA lender where you can actually settle and make payments.

It’s generally not my favorite way to do it because if you default on payments on an offer and compromise, they’ll keep all the payments that you’ve made previously and then just try to collect on the remaining balance.

I’d much rather see a borrower get a loan from somewhere else and pay off the SBA and owe that other lender money. So even if you default with that other lender, the savings associated with your offer in compromise are locked in.

Once you submit all this information to the SBA and you get a decision back, hopefully that decision is an approval. Many people want to know what kind of paperwork is associated with a settlement.

Believe it or not, what lenders do is all over the map. Some lenders don’t generate any settlement paperwork at all. And essentially what they’ll do is forward you a boiler plate template from the SBA stating that your settlement offer is approved on whatever the terms are that you approved and that needs to be made by a certain date. And that’s all that you get.

Larger lenders will often have a settlement agreement drafted by their attorney, which you would probably want to have your attorney look at as well.

This is a little bit more in depth and lays out all the specifics of the settlement, but it’s also typically the lender’s opportunity to have you basically indemnify them and admit that you were late and that this settlement is final.

And so many lenders will choose to go the “Settlement Agreement” route. I always prefer it, but I can tell you from experience that a lot of lenders are not willing to do that.

In some cases will ask if we can have the borrower’s attorney draft a Settlement Agreement at our own expense or have the bank’s attorney draft it at the borrower’s expense.

It’s good to have proof of any settlement and settlement payment. So I always recommend that everyone who settles keep a copy of all that where you keep all your important documents like the deeded to your house. The reason I suggest that is very often these loans are misclassified and end up getting referred to the US Treasury.

So if you settle your loan and you’re contacted by the US Treasury, it’s either one of two situations:

The SBA is improperly classified your settlement and basically the treasury didn’t get the memo. In those cases, all you need to do is send them the settlement documents and the proof that you paid it and that typically takes care of the problem.

The other scenario would be that the lender actually did classify the settlement correctly but with most of these settlements it does not include the release of the borrowing entity.

So in other words, if you borrowed through your LLC when we submit a settlement offer, we’re only offer in an offer in compromise for the personal guarantors. We’re not trying to settle the debt for the business entity.

And the reason is that business entity is now defunct and there’s really no value there. And so therefore it would make sense for you to pay out of pocket to settle that entity.

For example, if I have a business called “Jason LLC” and I personally guaranteed my SBA 7A loan for $300,000 when my settlement is approved, what I’m having released is my personal guarantee. “Jason LLC” is still on the hook and therefore the treasury still has the right to collect.

So if you get letters and calls to that entity, that’s fair game. Just keep in mind you’re not personally liable anymore, as you would have already settled your personal guarantee.

So that’s it folks. That is SBA offer in Compromise 2024 update.

The SBA is what I would call tough but fair. They’re willing to cut deals where it makes sense, but they’re certainly not giving away the store if they believe that you can repay your SBA 7a loan in full.

If you have any questions, you can schedule a case evaluation with me here and the fee for the case evaluation can be applied towards any future services should you retain me.

Thanks for checking out my website. If you enjoyed this article, I’ve got a hundred mores on my blog, and I’ve also got a YouTube channel with over a hundred videos (mostly EIDL related), I also am on Twitter with, and my handle is @EIDLadvice.