Hi folks! Welcome to my website. My name is Jason Milleisen. I’ve been helping SBA borrowers since 2008 (SBA workouts are all that I do). I know articles can be helpful, but nothing can replace a conversation. If you’d like to schedule a consultation, you can do so here. If you have questions about selling your business that has an SBA loan, I’d be happy to discuss your options.

I’ve written about this topic before, but I keep getting calls about it, so I figured it’s time to write about it again. So let’s set the stage: Your business is not doing well.

It’s got revenue, and it COULD be profitable if you didn’t have that pesky SBA loan payment. You’ve poured blood, sweat and tears into this business. Not to mention lots of your own money, even resorting to taking cash out of your IRA or 401K in order to avoid defaulting on your loan.

So what are your options?

I usually first answer this question by telling the borrower what they CAN’T do. The SBA Liquidation SOPs (Standard Operating Procedures) do state that a business can possibly settle under some very narrow circumstances.

But in PRACTICE? I have never seen a situation in 10 years of being a full-time SBA workout consultant where the SBA has allowed a business to operate while reducing the loan balance (not including bankruptcy). So in reality, if you want to keep your business open, an SBA Offer In Compromise is generally NOT going to be an option.

Can I sell the business?

Yes, you can sell the business. Keep in mind that 100% of the proceeds must go to the bank to pay down the loan balance.

Can the sale of the business count towards my SBA Offer In Compromise?

No, unfortunately not. Many people argue that if it weren’t for their efforts to sell the business, the business assets would only be worth a few thousand dollars instead of the several hundred thousands that the business will sell for.

While this may be true, the SBA doesn’t care. If you (or your advisors who lacks SBA experience) thinks you can negotiate this point, you will be sorely disappointed.

I’ve seen people play chicken with the SBA over this point, expecting that the SBA would blink. Guess what? The SBA didn’t blink. The deal fell apart, the SBA/Lender got peanuts instead of several hundred thousand dollars, the file was referred to the Treasury.

Did it make any sense at all? No, not in my opinion. But the SBA has a way of doing things, and they don’t like to deviate. When they talk about how you “can’t fight city hall”, this is exactly what they mean.

Governments and their employees have the luxury of being apathetic. It’s not their money, and they won’t lose any sleep over it. Just keep this in mind if you ever try to negotiate with them…just because it’s not fair or doesn’t make sense, it doesn’t mean that you can force them to bend to your will. Logic be damned.

Can I sell the business to a friend/family/business associate?

I’ve written an entire article on this particular topic.

The SBA’s general attitude is that sales should be “arm’s length”. This means that the buyer should be acting in their own best interests, and not doing it to help you settle your personal guarantee (Note: a personal guarantee can only be settle once the business has been sold or closed, and the assets liquidated – see below).

Many people tell me that other consultants advocate finding a “buyer”, have them hold that business for 12 months, then you can just buy it back later. That’s obviously misrepresenting the situation.

When I was a banker, we felt pretty strongly that this approach is fraudulent. If you have an idea like this, or maybe one where the buyer wants you to work for the business after you sell it to them (I’ve seen these get approved), the best thing to do is simply disclose it to your lender.

If the lender and the SBA are agreeable to the structure, then great, you are all set. But if they say no, then at least you’ve made an honest attempt to resolve the situation.

Can I open another business doing the same thing?

It depends. If you are a CPA, and plan to close, then re-open your business with the exact same customers, I would say the bank won’t like that (but honestly, would be hard for them to stop).

If you are a CPA, and you plan to start a new business offering the SAME services but with DIFFERENT clients, that’s acceptable. The intent of the SBA rules is not to limit your ability to work, but rather to ensure that if they are going to settle, that you aren’t going to benefit from the business financially going forward.

Will I be able to get another SBA loan in the future if I sell my business?

Whether or not you get another SBA loan will depend on how you handle your prior SBA loan(s). If you paid off your prior loans in full and on-time, that’s a good start. Of course, you’ll still need to go through the regular SBA loan underwriting process the next time around.

If you sell your business and settle your SBA loan through an Offer in Compromise, then that will render you ineligible for another SBA loan in the future.

The government keeps a list known as CAIVRS, which is essentially a “don’t give these people any more money” list. Not only will it prevent you from getting another SBA loan, it will also impact your ability to get FHA loans, federally subsidized student loans, and any other programs that involve the government lending you money.

As they say, hurt me once shame on you. Hurt me twice, shame on me. The CAIVRS list is the government learning that exact lesson.

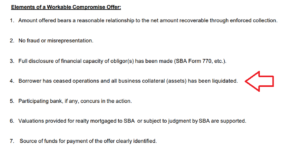

So once my business closes, I can just go ahead and sell the equipment?

No, no, no. And no. Do not sell any of your business assets without first getting express written consent from your lender! If you go and sell your business assets on Craigslist, without telling your lender, it could sabotage your entire Offer in Compromise.

The reason for this is that the lender could claim that you sold the assets for less than they were worth, and that if they would’ve sold them, they would’ve recovered more money.

So for this reason, any offer that you get for the equipment, present it to your lender in writing and ask them for a written approval. This will ensure that anyone looking at the transaction will be able to confirm that you got your lenders, okay, before going and selling the equipment.

What if I don’t have anyone to buy my equipment?

This is a common situation. People who have restaurants that have closed don’t necessarily know what to do with all of the kitchen equipment.

The good news is most banks have relationships with auctioneers who can come and value the equipment for the bank (it’s actually a requirement that the bank take an inventory).

These auctioneers often will have contacts that they can sell the equipment too. And if not, they can also put the equipment into what’s known as a “general auction”. Buyers who can purchase the equipment by making bids – highest bid get it.

Once the auction is over, the auctioner takes a commission and the balance is remitted back to the lender and applied to the loan balance.

What if my business assets aren’t worth selling?

There are situations where the equipment has no value. Anytime a business closes, the lender will typically send someone out to view the equipment, but if the equipment is low in value, a “desktop” appraisal can be done.

A “desktop appraisal” basically entails an appraiser taking a list of items (chair, tables, desks, etc), and assigns a value without actually seeing the items.

If you ran a service business such as a CPA, or something of that nature, chances are the only assets your business had was their customer list. Some desks, chairs, and computers.

In those cases, the lenders almost universally will abandon those assets. But again, you want to give the bank the opportunity to come and view those assets before you do anything.

Whatever you do, don’t throw them away without the banks approval! Let the lender see them first, so everyone is in agreement that they have no value.

If I can’t find a buyer, can I purchase the equipment for myself?

Generally that’s frowned upon. If you’re going be purchasing your own business’ assets, that could be an indication that you’re going start the same business all over again, which the SBA is generally not cool with.

With all that said, there’s no harm is asking your banker if they’ll allow that. If they say yes, be sure to get it in writing. I’ve heard my share of stories about bankers who make verbal promises to a borrower, only to leave the bank, or deny what they said.

I hope this article clarifies the issues that can arise when wrestling with selling or closing your SBA-funded business. If there is anything that I haven’t covered, feel free to schedule a case evaluation.