For the past 2 years, I’ve busted my butt trying to convince Google that when it comes to the topic of SBA Loan Default, I’m the top dog. Sure, you could argue that some of my competition could also be considered good resources for people seeking information about the SBA Offer In Compromise process.

But some of the results? Not a chance, my friends. Not a chance that the top results that are currently listed would ever be considered the best information available. You messed up Google. Big time.

I once had a marketing consultant tell me that Google’s main goal is for help people find all the answers to their question in one place. If that’s true, Google’s results for my top keywords confuse me.

Let me give you some examples. One of the top search terms for people seeking assistance with an SBA loan that they can’t repay is “SBA Loan Default”. My assumption is that if someone is looking for that term, they are looking for as much information as possible about how the process works. And not just general information, but rather, specific advice that can be applied to their own situation.

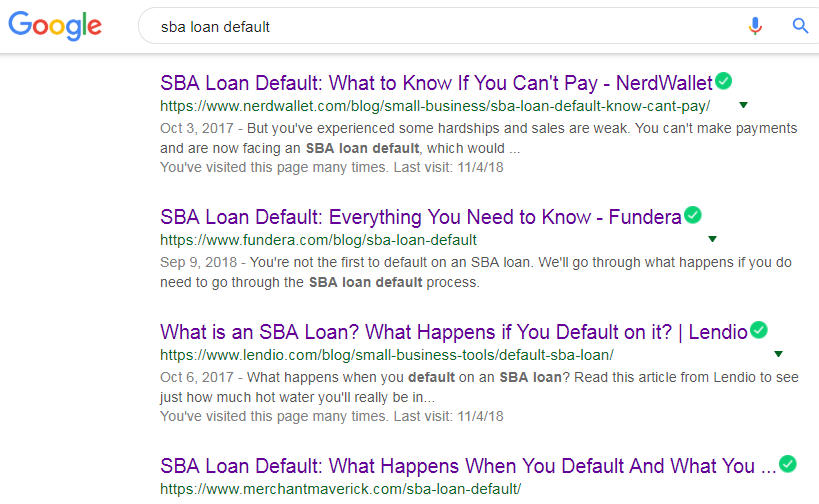

Here are the first 4 results of page 1 for the search term “SBA loan default”:

Let’s look at each of these results:

Nerdwallet.com

This article is painfully generic, and light on SBA-specific facts. Most of the information really covers the basics of any loan default, not just SBA. Things like that banks typically have a special department that handles defaulted loans, and that the bank will need to liquidate the collateral if a business defaults. Just when the article gets to the part about the SBA Offer In Compromise, the part that, you know, people are there to learn about, it just links to SBA Form 1150.

How on God’s green earth can Google believe that this is a good resource for people who are looking for answers to their SBA Loan default questions? Sure, Nerdwallet probably has a high authority ranking for financial information, but in this particular case, it clearly falls short.

Fundera.com

Fundera is a small business lender, and one of the types of loans they offer are SBA loans. Like Nerdwallet, they probably have great domain authority when it comes to small business finance. And I’m sure they some amazing in-house SEO people whose job is to get them noticed. But expertise when it comes to SBA loan workouts? I think not.

This article is, in my opinion, better than the Nerwallet article. But like Nerdwallet, this is an article about what could happen. It’s very light on exactly how to get an Offer In Compromise approved.

My favorite part is the link to the Offer In Compromise is wrong: it links to the IRS Offer In Compromise page, which is NOT the same thing as the SBA Offer In Compromise. Yet this article, according to Google, is the 2nd best article available on this topic? Come on Google, you’re better than that!

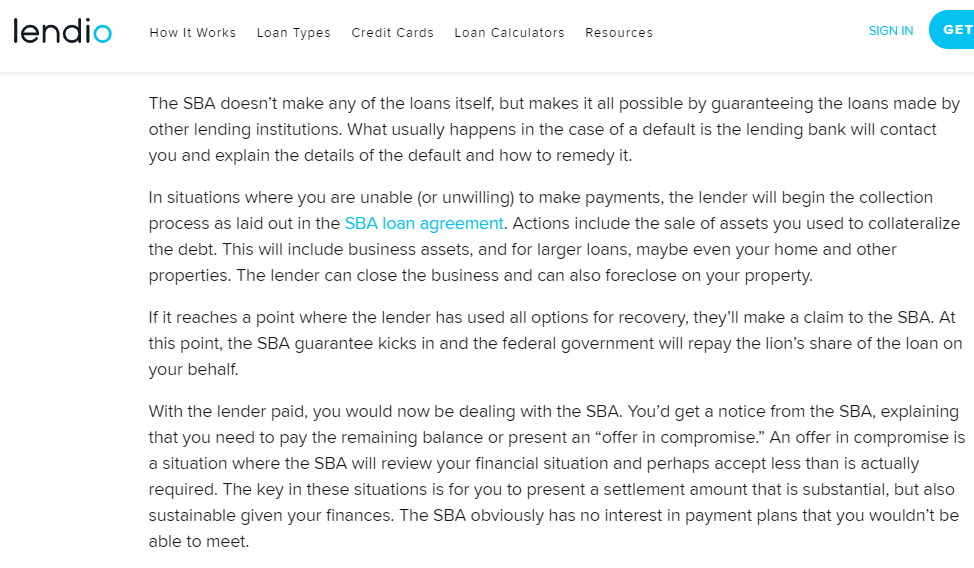

Lendio

They are a lender. And clearly don’t know a lot about the topic of SBA loan default. How do I know this? This article has 8 short paragraphs, and 2 of them contain inaccurate information:

Factual Error #1: “If it reaches a point where the lender has used all options for recovery, they’ll make a claim to the SBA.”.

The lender may request payment under the guarantee once a borrower is 60 days past due. It has nothing to do with whether the lender has used all their options for recovery. The writer is confusing this with the wrap-up report. The wrap-up report is when the lender refers the file to SBA because they have exhausted all recovery efforts, and any further action would be cost-prohibitive (i.e. sue a guy who has no money).

Factual Error #2: With the lender paid, you’ll now be dealing with the SBA.

Survey says: WRONG! You will deal with the SBA once the lender closes their file and refers it to SBA. Payment of the SBA guarantee is NOT the triggering event. In many cases, lenders actually insist on waiting until the SBA reimburses them before they will engage in OIC discussion.

So there you have it, ladies and gentlemen. The 3rd best option in the whole world has material factual errors in 2 out of 8 paragraphs. Care to explain, Google?

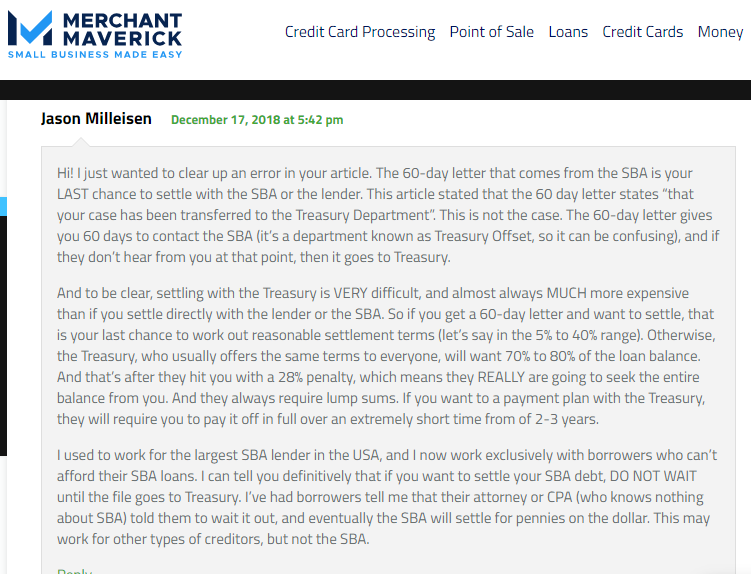

Merchant Maverick

Google’s 4th pick for “SBA Loan Default” also contains errors. I actually commented on what was wrong their article right on the site:

In a world of infinite things to Google, I get that Google’s algorithm simply can’t understand every nuance of every topic, so they relay on other factors which may be less than 100% accurate. But in my case, it’s potentially costing me tens or hundreds of thousands of dollars, which is why I frequently whine to anyone who will listen about how Google is totally screwing me.

If anyone reading this article has any insights about what I can do to show Google that it’s me that the authority here, I’d love to hear from you!