Welcome! If you have lots of questions about SBA loan default and forgiveness, I have many of the answers in my Definitive Guide to SBA Loan Default and Offer In Compromise. If you just want to know about the tax thing for now, read on. If you prefer to listen rather than read, I also have a podcast that covers many SBA default and forgiveness questions.

Note: The writer is not a CPA or tax professional. This article is for general information purposes, and should not be construed as tax advice. Readers are strongly encouraged to consult their tax professional regarding their personal tax situation.

There’s no doubt about it: negotiating an SBA loan settlement can be taxing.

These days, lenders are so overwhelmed with defaulted loans that it can take an act of Congress to get them to even return your phone call. Then, when they do return your call, they ask you to fill out a series of onerous and confusing forms.

Once you return that info, it’s likely that your initial attempt as a settlement offer will be summarily dismissed. From there you negotiate, fighting tooth and nail in order to get a deal done. Finally, after weeks or even months of mind-numbing, energy-sapping negotiating, a deal gets done.

You send them a check, and finally breathe a sigh of relief. After all, the situation is now over and behind you right?

Well, not exactly. At least not according to the folks at the IRS.

What, what? Why isn’t it over?

Debt forgiveness, you see, is treated as taxable income. Why?

In a nutshell, if someone gives you money and you don’t have to pay it back, it’s taxable. Just like you have to pay taxes on wages from a job.

Part of the reason that debt forgiveness is taxable is because otherwise, it would create a giant loophole in the tax code. In theory, your boss could “lend” you money every 2 weeks, and at the end of the year they could forgive it and none of it would be taxable.

Is this negotiable?

I’ve had clients ask me to try to negotiate the tax consequences of debt forgiveness. Unfortunately, no lender (including the SBA) has the ability to do such a thing.

Just like your employer is required to send a W-2 to you every year, a lender is required to send 1099 forms to all borrowers who have debt forgiven. With that said, just because lenders are required to send 1099s doesn’t mean that you personally automatically will get hit with a huge tax bill. Why?

In most cases, the borrower is a corporate entity, and you are just a personal guarantor. I know that some lenders only send 1099s to the borrower (that’s what we were instructed to do at the lender I worked for). The impact of the 1099 on your personal situation will vary depending on what kind of entity the borrower is (C-Corp, S-Corp, LLC, etc). Most CPAs will be able to explain how a 1099 would manifest itself.

Help me out here Jason! Is there any way around this?

Maybe.

The IRS does have an insolvency exclusion. If a borrower is insolvent (basically defined as having a negative net worth prior to the debt forgiveness), then you may not have to pay tax on SBA debt forgiveness. I’ve taken it directly from the 2018 IRS instructions:

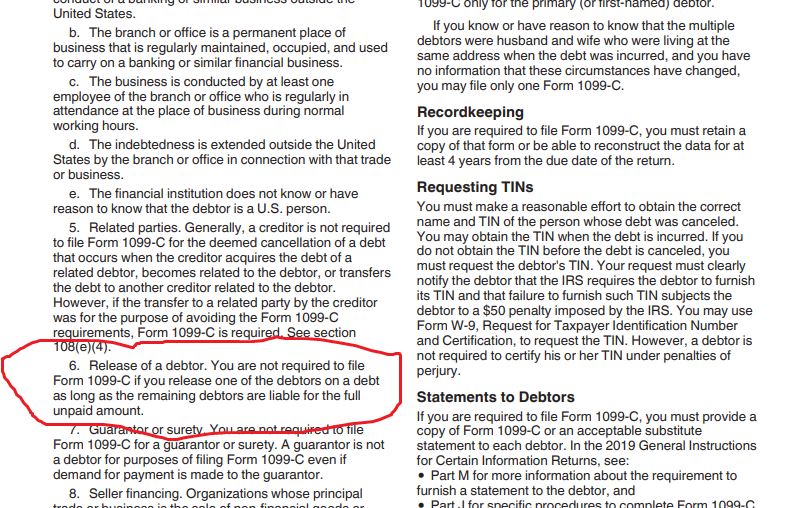

Another possible way around it: if you are simply released as a guarantor, and others remain on the loan, the lender doesn’t need to send you a 1099. I found that in the IRS 1099 Instructions. It makes sense if you think about it. If you are one of 10 guarantors, and the bank is still going to get paid in full, it wouldn’t be fair to make you pay tax on it. Here’s the exact language from the IRS:

The final way that I’ve heard about a 1099 not being a complete disaster is by offsetting it against any losses you incurred while owning the business. I have no idea if that’s valid, but I once had a client tell me that’s exactly what his tax guy was going to do.

He bought the business for $500K, and was worth $0 when the business closed. He called that a $500k loss. So even if $500k was forgiven and resulted in a 1099, it netted out to $0 in taxable income.

Might Still Be Best Alternative

I have a favorite phrase that I use with my clients. When it comes to loan forgiveness, there are typically no “good” options. You are simply trying to pick the best “bad” option.

This tax question is a good example of choosing your best bad option. Let’s pretend for a moment that your SBA Offer in Compromise was just approved.

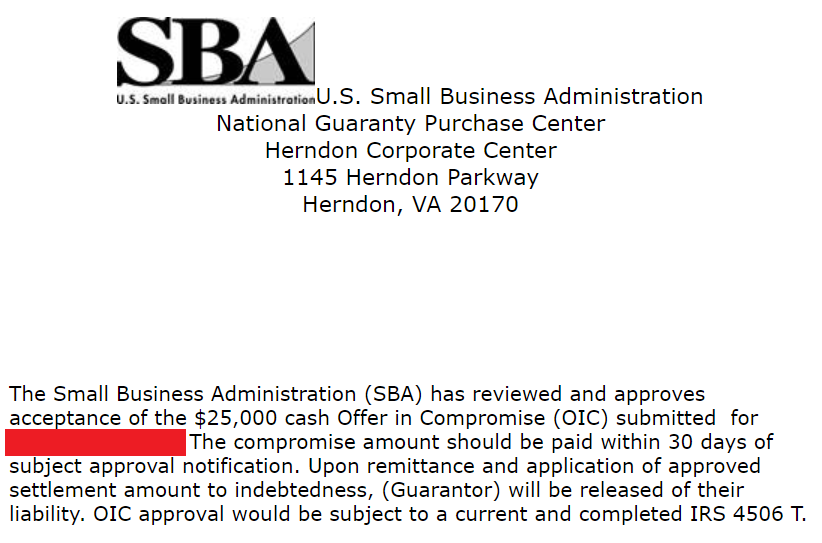

Let’s say you owe $239K (this is based on an actual OIC that was recently approved). You hire a crackerjack consultant like me and BOOM, the SBA approves a settlement for $25,000. AWESOME!

Settlements that are reached directly with the SBA are communicated with a simply email. Here is the actual email from the SBA for a the recently approved OIC. This approval resulted in the SBA forgiving $214K ($239K balance, settled for $25K).

Not surprisingly, this is always an exciting and emotional moment for my clients.

It’s the culmination of a emotionally trying few years. You labored through 12-hour days. Your investment in the business evaporated into thin air. After many sleepless nights and no paycheck, you made the heart-breaking decision to throw in the towel. Then finally, you suffered through the fire sale of the assets, where the $14,000 pizza oven sold for $2000.

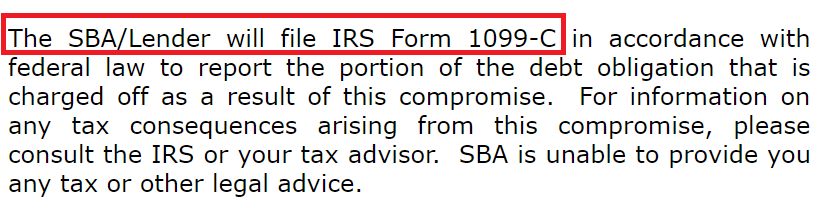

When word of an approved settlement arrives, it’s pure euphoria. Finally, something has gone your way. That euphoria is often short-lived when they read one particular section of the OIC approval:

Time to Pick the Best “Bad” Alternative

So here are the scenarios you are facing:

- Accept the settlement and get a 1099 – If you were the client who was approved for the $25,000, you’d be looking at paying the $25,000 plus taxes due on a $214K 1099. Assuming a tax rate of 30%, that would mean federal tax liability of $64,200. Total cost: $64,200 + $25,000 = $89,200

- Accept the settlement and a 1099 never shows up – When I worked for the largest SBA lender in the country, we were very confused about when to issue a 1099. If we were confused it would not shock me if others were too. If your lender simply doesn’t send you a 1099, or if they determine that a 1099 is not warranted (perhaps because you were one of several guarantors) then there will be nothing to report. Total cost: $25,000

- Pay off the loan in full – Total cost: $239,000.

- Decline to settle (part 1) – If you decide that the cost of the tax bill is too much, you can skip the settlement. The file will get referred to the US Treasury. They will add 28% to your loan balance, and if you have a job, get a federal tax refund, or collect social security, you’ll have to worry about garnishment. Total cost: Unknown, but the balance owed will jump from $239k to $306K.

- Decline to settle (part 2): One final possibility: even if you decline to settle, it’s possible that you’ll get a 1099 anyway. I’ve gotten calls from borrowers who didn’t settle, never heard from their bank, and still received a 1099.

So there you have it. All of the above options suck. Now you have to decide which one sucks the least.

Jason,what do most of your clients do?

Most of my clients go ahead with the settlement. In fact, I can’t think of any client not settling due to 1099 concerns in my 9+ years of doing this. Given all the possible ways that SBA forgiveness may not result in severe tax consequences, they decide to settle the debt to ensure there is no further collection action against them. Many also reason that even if the worst happens, paying the tax on the forgiven portion is still better than paying it in full.

With so much money on the line, you don’t really want to assume anything one way or the other when it comes to tax implications of a settlement. Do your homework, talk to you tax professional, then make an informed decision.

Have questions beyond the tax thing? Please read on…or check out my podast.

Common Questions About SBA Loan Forgiveness, Part I

Is it possible to settle an SBA Disaster Loan?

It is possible to settle an SBA disaster loan. It should be noted, however, that disaster loans are handled by a different area than “regular” SBA loans. Technically, they have the same SOPs (standard operating procedures), but the rules tend to be interpreted a little differently by the disaster loan folks than they are by the “regular” SBA loan area.

How long will it take to settle my loan?

It depends. There are many factors that can drag out the process.

Is there business equipment that needs to be sold?

Is there real estate that needs to be sold?

Are you dealing directly with the SBA, or is your lender still servicing the loan?

Like a construction project, the rule of thumb is that it will always take longer than you expect it to. With that said, don’t despair. It is possible to settle.

The SBA is fair (in my opinion), so if you abide by the settlement rules, and understand how the SBA is going to evaluate your offer, your chances of settling are good provided you can raise an acceptable amount of cash.

What can an SBA workout specialist do for me that I can’t do for myself?

A knowledgeable SBA workout expert will have a strong knowledge of the SBA settlement process. They will have a firm grasp of how the SBA will analyze your financial situation in order to determine whether your offer is acceptable.

In addition to their ability to determine a fair settlement offer, an SBA workout expert will be able to challenge lenders, who often hide behind the SBA as an excuse not to settle. Some lenders will cite specific SBA guidelines as reason why an offer cannot be acceptable.

A seasoned SBA workout pro knows the SBA rules, and can challenge the lender when they know that something is not factually correct.

As a business owner who is going through the settlement process for the first time, how could you possible know all the SBA rules and practices? More importantly, how would you know if they lender is accurately interpreting the SBA guidelines?

Seeking more answers? Here is the entire article of common questions (part 1) and here is part 2.

Distressed Loan Advisors (http://www.JasonTees.com) offers expert advice about dealing with SBA Loan Default and Forgiveness, and can be reached at . or ..