Are you seeking a comprehensive step-by-step guide to parlay your SBA loan default into a successful SBA offer in compromise? Please go here.

Let’s say your business has closed, and you owe a ton of money on your SBA loan. It’s only natural to wonder: how do I get out of my SBA loan? Is there such thing as SBA debt forgiveness?

In this article, I’m going to tell you all the factors that are present in an “ideal” SBA Offer In Compromise scenario. Do all these factors need to be present in order to successfully navigate the SBA Offer In Compromise process? No. And honestly, very few cases do. But the settlements that do have every factor? Those are among the best settlements that I’ve negotiated for my clients.

1) Home Equity

Whenever a prospective customer calls me to discuss their SBA loan default, one of the first questions is whether they pledged their home. Regardless of the answer (I’ll explain why in a moment), the next question is whether there is any equity in it. To your bank and the SBA, one of the easiest ways to recovery their loan principal by way of your home equity.

So, why do I ask how much equity you have regardless of whether you pledged your home as collateral for your SBA loan?

If you DID pledge your home as collateral, having equity in that home can sink an Offer In Compromise before it even starts. Why? Because the SBA is very clear: if a pledged home has equity in it, and settlement offer should START at that amount. So it won’t be less, but it could definitely be more.

If you DID NOT pledge your home, you are not necessarily out of the woods. When you have equity in your home, the bank expects you to borrow against it. If you claim that you don’t qualify for a home equity loan or a refinance, they may ask for proof that you applied and were declined.

One other tidbit worth noting: as I wrote about here, it’s possible for a bank to place a lien on your even if you didn’t voluntarily grant one.

Calculating Home Equity

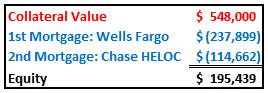

Also, if you’re wondering if there is a formula for determining equity, there is….kind of. The general idea is to take the “collateral value” of the home, then deduct the the mortgages that have liens position that are senior to the SBA loan. Here’s a simple example:

I said “kind of” in the paragraph above because the definition of “collateral value” varies from bank to bank. It might be easier if we establish some definitions:

“Market Value” = The amount you can sell your home for in a normal situation.

“Collateral Value” aka “Liquidation Value” = The amount that that remains after a foreclosure or forced sale. It takes into account the costs of foreclosure like attorney fees, court costs, and realtor fees. There is also a term called “foreclosure stigma” which drives down the value of a home. If a home is foreclosed upon, the theory goes, then buyers will be looking for a deal. Since bank wants to sell the as quickly as possible, it results in a lower price than market value.

Contrary to what you may think, banks DO NOT want to own real estate. Not to get all corporate finance on you, but one measure that investors use is Return on Assets (ROA). Foreclosed real estate that the bank owns is basically a non-performing asset. The more non-performing asset that they have, the lower the ROA.

Ideal Scenario: Don’t own a home. Or own home that is not pledged, and contains no equity.

2) Liquid Assets

Cash is king. That’s a line we’ve all heard at one point. And it holds true in this instance as well. First and foremost, when your lender is trying to get their money back, they will look for cash or cash equivalents. Makes sense, right? But it should be noted that not all liquid assets are born equal.

Checking, Savings, CDs, Stocks, Bonds etc.

Cash in any of these accounts is super easy to identify. And if it’s plentiful, they’ll want it. So if you have $100K in your personal checking account, and you owe $50K, prepare to pony up. The good news is that the SBA will consider other factors. If you are unemployed, for example, it can be argued that you need some (or all) of your cash to pay your mortgage or other required expenditures.

Retirement Accounts – 401K or IRA

At some point, someone decided that it would be a good idea to protect people’s retirement funds. For that reason, creditors cannot levy designated retirement accounts. By “designated”, I mean it must actually be in a protected account (401k/IRA). Just declaring the money in your savings to be for retirement won’t work.

While these assets are protected from creditor levies, it’s a common method of raising cash to fund SBA OICs. Not ideal, but often the only asset borrowers can tap for some quick cash.

Ideal Scenario: It’s better if you don’t have any (duh), and you need to borrow from friends or family to fund your settlement. If you do have liquid assets, being held in levy-protected account will help during an OIC negotiation.

3) Earning Potential

When evaluating your Offer In Compromise, the key idea is to determine if your SBA loan default is due to financial hardship. Simply put, can you afford your SBA loan payment? So obviously, they look at your income. But they don’t just focus on your current income. They also focus on your income potential. This is why it’s difficult for a young doctor or a lawyer to settle. Even if you can’t pay right now, they also consider your future earning potential.

I’ve often had the conversation with clients about their job search, specifically regarding the timing. As you might assume, it’s much easier to settle when the borrower has no income. Of course, the reality is that people need to pay bills, so the timing of when you take a job can’t always be helped. Besides, it not about deceiving the bank. If you are on the verge of landing a job, that should be disclosed. But yes, it would definitely make the OIC process easier if you are unemployed.

Also related:

Profession. Banks give me a hard time when my client have a background in law, finance, or medicine. The reasoning is obvious, people in those professions do well financially. Not something you can help, but it’s a thing.

Age: The younger you are, the more earnings you have ahead of you. And the older you are…well, you get it.

General Health: If you not healthy enough to work, that impacts future earning potential.

Ideal Scenario: Unemployed from a low-paying profession while old and sickly.

4) Personal Cash Flow

Let’s assume you do have a job. That’s fine. There is no specific income level that will disqualify you from an OIC. The bank needs to believe that you are experiencing genuine financial hardship. That term is fairly subjective, but I’d define it as a situation where your income cannot support your modest and reasonable expenses. In case you were wondering, “modest and reasonable” excludes vacations and jet skis. Think mortgage payments and groceries.

If you have a job, the bank will compare what you currently make versus your monthly expenses. If you have excess monthly income, the bank may want monthly installments. They may also push you to borrow a lump sum, and make the payments using your excess income.

Ideal Scenario: Deficit personal cash flow.

5) Access To Capital

Once a month, I explain the entire OIC process to a potential customer. It all sounds great to them. Until I ask them how much they can raise to settle.

“Oh, I’m completely tapped out. I’ve borrowed from everywhere and everyone I know. I put all my savings, including my retirement, into the business”.

Ugh. Bad answer. It’s not a negotiation unless you have cash to offer (lump sum preferred). You can’t expect to recity an SBA loan default if you have nothing to offer. While it’s fine (and normal) to not have any personal liquidity, you need to be able to raise some cash. By far the most common way to do that is borrowing from friends and family.

Ideal Scenario: No liquidity, but with the ability to borrow.

Summary

Do you know those amazing results I tout on my testimonials and results page? Most of them had the majority of the characteristics noted above. Most of these clients:

1) Didn’t own a home, didn’t pledge their home, or pledged home that had no equity;

2) Had nominal liquid assets;

3) Were unemployed or experienced significant personal cash flow deficit;

4) Had access to capital with which to settle, typically via retirement savings or loans from friends and family.

You can’t always help your circumstances, but it can never hurt to understand what circumstances can contribute to a successful SBA Offer In Compromise.