Don’t feel like reading? This article is available in Podcast form:

Hi folks! Welcome to my website. My name is Jason Milleisen, founder of Distressed Loan Advisors. I’ve been helping SBA borrowers since 2008 (SBA settlements are all that I do!). I know articles can be helpful, but nothing can replace a conversation. If you’d like to schedule a consultation, you can do so here.

The most asked question that I get, along with how much my services cost, is how much do I think a guarantor can settle for.

To answer the question from the title, no, to my knowledge, there is not a formula that determines how much you will be able to settle your personal guarantee.

With that said, I do tell my client’s that based on their personal financial situation (SBA Form 770), I will give them an approximate range of what I would expect them to settle for.

But why can’t you simply write a formula that will spit out a single definitive number?

Mostly, because the amount you will ultimately settle for will depend on the bank and the workout officer and the bank you are negotiating with. Since different banks will be tougher to deal with than others, this is why I can’t give you a specific number when it comes to your settlement.

What I will do, is go over your entire situation (sssets, liabilities, income, expenses, age, health, earning potential etc) and explain how bankers might view your overall situation. Determining the amount of the SBA Offer In Compromise can be considered part art, part science. And as with art, there is no set formula.

So what types of things will different banks look at differently?

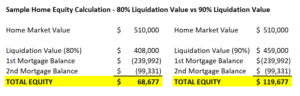

1) Determining equity in your home. Banks will usually apply some sort of discount to your home value. Some banks will apply a 10% discount. Others apply 20%. This can swing the amount of your OIC offer pretty significantly. So can the appraisal – the appraised value is not up to the bank – but it’s definitely a factor.

2) Your future earning potential. As soon as some banks see that a business owner is a doctor or a lawyer, they will often assume great earning potential. Other banks will take the time to understand that not every doctor or lawyer makes a million dollar per year. And to get a little touchy feely, some people realize that being a doctor or a lawyer doesn’t make them happy, and they want to try something else.

3) The stuff that doesn’t show up on your PFS. When I worked for a bank, we had a borrower who send us PFS after PFS that showed no income, no assets. Yet, the bank management refused to settle.

And it had nothing to do with what was on SBA Form 1150. It had to do with the fact that the bank believed the borrower’s family had money, and they were determined to play hardball until some of that money appeared.

Obviously this is part of the OIC review process that you’ll likely never be privy to, but for some guarantors, it’s as real as cash in the bank.

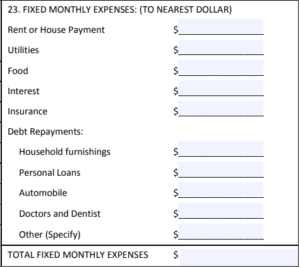

4) Your monthly excess income. The PFS has sections devoted to listing your income and your expenses. Many expenses can be sliced and diced depending on their definition of what a discretionary expense is. Some banks carve down expenses to the bare minimums, while others are more liberal.

So those, folks, are the reasons why I can’t give you a down-to-the-dollar estimate when you ask me how much you’ll be able to settle for!

If you’d like to learn more about the SBA Offer in Compromise process, I’d suggest starting with the 33 most common questions I get about SBA Offer in Compromise.

While I can’t predict with certainty the amount that you’ll be able to settle your SBA debt for, there are a few things that I can predict!

There Are No Free Passes

If you have nothing to offer for your SBA OIC, there is nothing to discuss with the SBA. The Offer in Compromise is a negotiation based on the lender/SBAs assessment of their best recovery option. It’s a business decision.

In other words, they aren’t settling to be nice or generous. They settle when it makes sense from a business standpoint. Does the OIC sitting in front of them represent the best possible recovery? Are there any other avenues that could potentially result in a materially greater recovery?

When you offer them $0 in exchange for something extremely valuable (your personal guarantee), there’s really nothing for them to consider.

Settlements Are Not A Lottery

If you think you’re going to slip an unreasonable offer past your lender or the SBA, think again. Throwing a silly offer against the wall in hopes that it will stick is like counting on lottery winnings to carry you through retirement instead of saving in your 401k.

The SBA Offer in Compromise is designed for situations when the guarantors don’t have the ability to repay their debt in full from personal assets.

If you owe $125K, and have $500K sitting in your bank account, no portion of your SBA loan will be forgiven. Period. Full Stop.

The SBA Doesn’t Care About Ownership Percentage

It doesn’t matter if you owned 100%, 50%, or 0% of the business. If you signed an unlimited personal guarantee, the SBA will expect you to pay as much as you can afford, even if that means paying the loan off in full.

Over the years, I’ve had lots of partners come to me asking if there is a way for them to just pay “their half” since they only owned 50% of the business.

The only way this would be possible would be if your personal guarantee was limited to 50% of the loan amount. You can check your loan documents to determine this, but in my experience, the vast majority of personal guarantees are unlimited.

There is a specific reason why the SBA typically takes unlimited personal guarantees from all owners of 20% or more: this ain’t their first rodeo. They know that partnerships fall apart, and one of them is often left holding the bag. They just don’t know who’s going to split, and who’s going to stick around.