Anyone who has ever started or purchased a business knows the rush of adrenaline you get at the beginning. This tiny seed of an idea has finally broken through the soil. Beyond that? Sky’s the limit!

Your head swirls with ideas that will make your business thrive. A birthday club! A loyalty card! A new twist on an old product! Online sales! Pictures of your customers on the walls!

The possibilities are endless, and with these kinds of ideas, it’s not really a matter of whether your business will make money. It’s simply a question of how much. Yes, it’s fair to say that optimism is radiating from every fiber of your being.

Let’s pump the brakes for a moment.

If it’s your first venture, let me assure you of something. This phase of any business venture is like the honeymoon phase of a marriage. It’s not about reality. It’s all about dreams, passion, and possibilities.

And just like a honeymoon phase in a marriage, at some point certain realities will set in. That’s what I’m going to talk to you about today: the realities, and more to the point, the obstacles that you may face once you are knee-deep into a business that has an SBA loan.

1. Understand What A Personal Guarantee Means

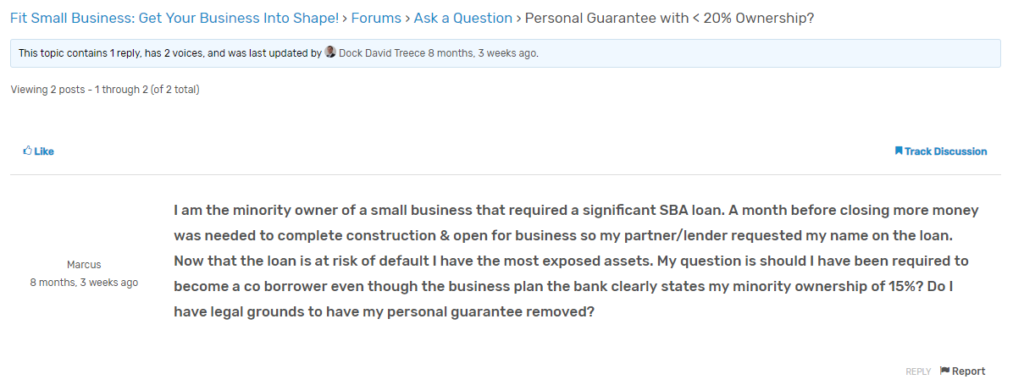

Yesterday, I was looking around the internet for forums and articles pertaining to all the major keywords and phrases people use to find me. I do this routinely in hopes that wherever people are looking for information about the ugly side of, they’ll find me.

Upon locating a site called Fit Small Business, I found a question about the SBA personal guarantee. I took a moment to read it, and noticed something pretty unsettling. Here’s the question, and then the answer from the moderator:

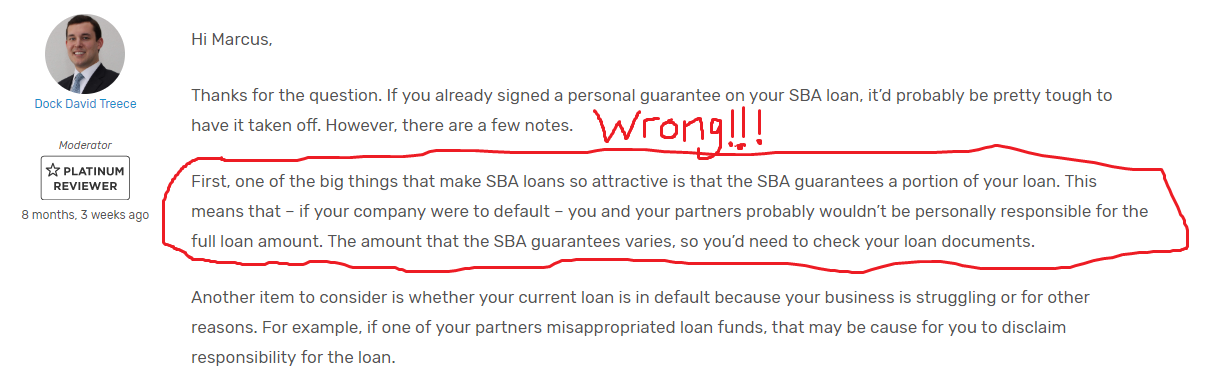

In case you missed it, the part I that’s circled in red and wrote “WRONG” above is the unsettling part. A small business website, who created this forum to answer questions from business owners, got this completely wrong.

For the record, the SBA guarantee absolutely does NOT mean that the SBA pays off 70% of your loan. I wrote about this years ago because some borrowers thought the same thing.

It’s one thing for borrower to not understand. But for a site like Fit Small Business to get it that wrong? Not only does that give this one person completely wrong info, but it could give a potential borrower bad information that they might actually make a decision.

Even worse, despite making it look like people could comment, when I attempted to correct the moderator, the comment didn’t post.

So, just to set the record straight:

- The SBA guarantee is for the lender only. It reimburses them for a portion of the loan, assuming certain criteria are met.

- Even if the bank is reimbursed, it doesn’t change the legal balance owed by the borrower and guarantors.

- The guarantee fee that a borrower pays at the beginning of the loan is paid because, in theory, the SBA loan was given because credit was not available elsewhere. In other words, you pay them a fee, and they promise to minimize the bank’s loss in a default situation.

- When you give a personal guarantee, you risk the bank pursuing you for your personal assets.

2. Understand What Pledging Your Home Means

When a bank asks you to pledge your home as collateral, it means that if you default on the loan, you could be at risk of foreclosure.

Some borrowers think that their SBA lender can’t foreclose if there is a 1st or 2nd mortgage in front of the SBA loan. This is not the case. It simply means that the foreclosing lender would need to pay off any liens that are senior to them.

In some cases, this represents an unattractive option for an SBA lender. Let’s say a home is worth $500K, and the SBA lender has $475K in mortgage ahead of them. Most banks wouldn’t pursue the home since, after paying off the other lender and costs of foreclosure, it wouldn’t yield any cash.

On the flip side, if your home is worth $500K, and your 1st mortgage balance is $100K, your SBA lender will have a significant reason to consider foreclosing.

To be clear, banks are encouraged by the SBA to avoid foreclosing on people’s home. If you have equity in your home, they’ll be glad to take a check in lieu of foreclosing.

3. Past performance is no guarantee of future success.

There is tons of data available about how well franchises funded with SBA loans fare. There is a company who sells this information to lenders, who use it to weed out franchises with poor track records. It’s known as the Coleman Report.

As most entrepreneurs with franchise experience know, they can also get lots of good info from the FDD (Franchise Disclosure Document).

Despite all that good info, taking on a franchise does not come without risk. In my opinion, many would-be entrepreneurs are lulled into a false sense of security by great stats and tales of success.

If they tell you that 95% of all franchises ever opened are still in business, but sounds great. But it can also be misleading. Are those franchises in your area, or would you be the first? Competition for authentic NY style pizza in NYC is going to be greater than in Toledo Ohio.

Is the concept relatively new? Or is has it been around for a while? I remember that 5 years ago in my town, there were 6 different frozen yogurt shops. Today? There is 1. When a new trend emerges (like high quality fro-yo), lots of entrants rush into the market. Inevitable, a shakeout happens and not everyone survives.

Finally, do you know really, truly what you are walking into? If you’ve never worked retail, do you fully understand the implication of 80 hours weeks on your family and your body? Guys like me who come from the corporate world often are shocked at how hard it is to make the transition.

4. Closing a business doesn’t necessarily mean you are free of the franchise

I have a client who closed her business, thinking once the business ceased operations, so would any obligation to the franchise. Unfortunately, this was not the case. Her franchise agreement called for payment for several more years.

Once she discovered this fact, we went to the franchise to negotiate a settlement of that agreement. Luckily for her, it ended up being a few thousand dollars. For some franchises, it could be significant;y more depending on the length of the agreement and minimum monthly remittance that’s required.

Conclusion

I’m not saying that buying into a franchise system is a bad idea. I do believe, however, in looking before you leap. Understand the risks so that you can make an informed decision. If things go bad, and you understood that was a possibility from the start, then hey, thems the breaks.

But to walk into a business without understanding the terms you’ll be bound by? That, my friends, is a recipe for disaster.