It was never supposed to go like this. When you took that SBA loan, life was on the upswing. Sure, there might be some bumps in the roads, that’s to be expected. But the mess you’re in now? You never signed up for this.

As much as you fought to keep your business afloat, it just ain’t working. The harder reality? You’ll never be able to repay your SBA loan.

So now what? You probably have questions.

Does the SBA forgive loans? Yes, but with lots of caveats.

And that’s the purpose of this article. To walk you through the major features of the SBA loan forgiveness process following a default.

Business Must Be Closed (With A Caveat)

On more than one occasion, I’ve have SBA borrowers comes to me having already perused the SBA SOPs. As a result, they know enough to make them dangerous. They’ve ingested some information, and think that they understand the process.

But here’s the thing: what’s written in the SBA SOP is open to at least some subjectivity. You might think it’s funny that such a numbers based decision could have some subjectivity, but it’s true.

When it comes to the issue of the business closing, you would not be wrong if you stated that Form 1150 is actually contradicted by the Liquidation SOP. Let me show you.

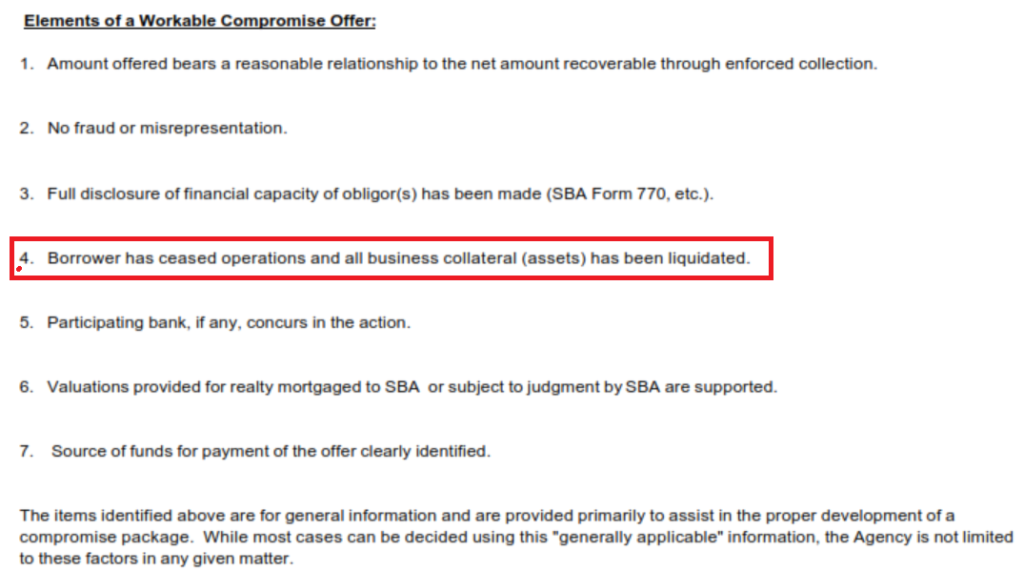

Below is a screen shot from SBA Form 1150. It’s on page 2 (for those who care), which outlines “Element of a Workable Compromise”. It’s pretty clear what they want. The borrower needs to cease operations.

But, wait, there’s more!

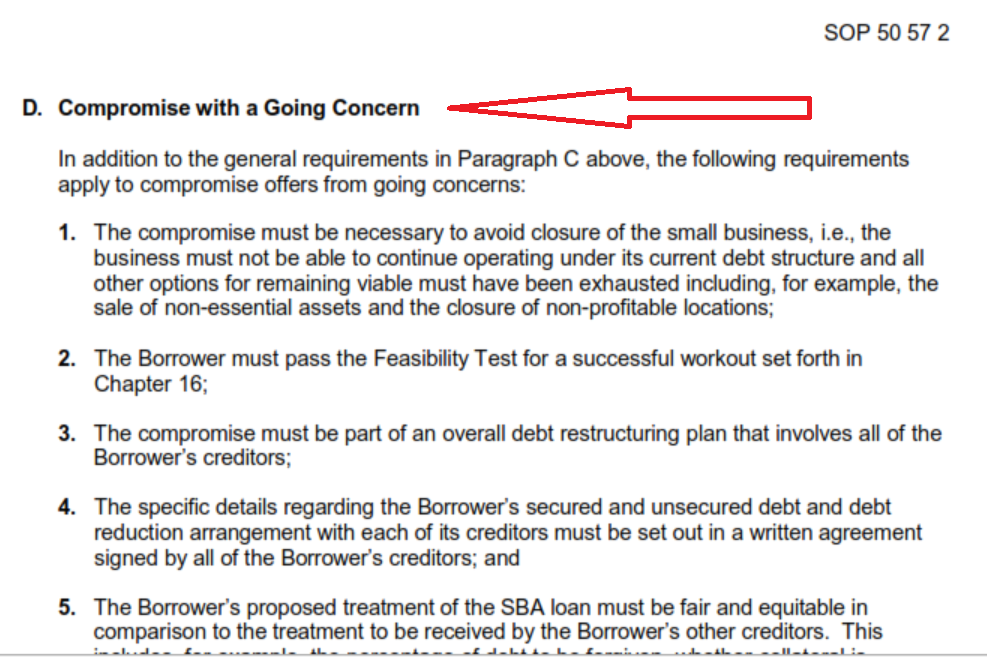

The SBA throws a wrench into the whole thing with the information outlined in the screenshot below. “Compromise with a Going Concern” has a section within the SBA Liquidation SOP.

Going Concern means that we are assuming the business will continue to operate. So, contrary to the Form 1150 instructions, this is saying that it is a possibility.

I’ve broached this subject before with the SBA.

One time, my borrower said he’d close the business as long as he knew the SBA would approve the OIC. They immediately rejected the OIC, stating they wouldn’t consider it because the business was still operating.

So the next time, I referenced the screenshot above, and asked under what circumstances a business would be able to settle while remaining open. The answer: it needs to be treated like a bankruptcy. I interpreted that to mean that if the SBA were going to consider it, all other creditors would also need to agree to the same discount as the SBA.

Just to give you an idea of the likelihood of such a scenario, I can’t recall ever seeing it. I’d venture to say that getting ALL your creditors to settle for the same percentage of the total is fairly unlikely. This is why we don’t see it very often, and why it’s unlikely that it will be a realistic option for the typical borrower.

Proceeds From the Sale of Your Business Assets Cannot Be Used To Settle the SBA Loan

If you look at the screenshot from the SBA Form 1150 I talked about earlier, the same element of a workable compromise (#4) that I mentioned also states that business assets must be liquidated.

On more than one occasion, I’ve had borrowers come to me and say “I don’t have any cash of my own, but I can probably get $20K for the equipment. Would that be enough to settle?”

Unfortunately, it doesn’t work that way. Since the business assets are almost always pledged as collateral, the SBA will require any proceeds from the sale of those assets to be applied to the loan balance.

The bottom line? If you want to settle your personal guarantee, you’ll need to fund it from personal assets.

Thought that was bad? You are going to hate this next part.

Let’s set the table with an example:

You purchased a franchise called Jason Juice a few years back. You work 12 hours per day, 6 days a week, all while losing money hand over fist. Its just not working, no matter how hard you try. With a heavy heart, you decide to call it. Closed for business.

You’ll lose your investment in the business. That goes without saying. To make matter worse, you still owe the bank $300K.

Determined to knock that $300K down as much as possible, you list the business for sale. The process is a real pain. People coming to the store to kick the tires. Unending lists of questions. And the low ball offers. Oh my, the low ball offers.

After months of this, you finally get an offer for $150K. Not a full payoff, but orders of magnitude better than the $25K offer you got for the equipment.

Your lender and the SBA stand to recover an additional $125K due to your hard work. That must worth something to them, right? So, you decide to try to use this new-found leverage.

You make a seemingly reasonable proposal: You’ll agree to sell the business for the $150K, and in exchange the bank and the SBA forgive the remaining balance.

If you do the math, your offer makes all the sense in the world. They can net $150K from a sale, or they can maybe net $50K if you just sell the assets ($25K), then go through the OIC process to get your personal guarantee released ($25K, max). An easy business decision, right?

Smart business decision or not, SBA loan forgiveness doesn’t work like that.

If you sell your business as a going-concern, all those proceeds must also be applied to the loan balance before any level of SBA loan forgiveness can be contemplated.

Crazy? I wholeheartedly agree.

Using the sale of your business as an SBA loan forgiveness “bargaining chip” is completely logical. And if I didn’t have 10+ year of experience helping customers, I’d push that strategy too.

The SBA Guarantee Does Nothing For You in a Default Situation

I’ve written about this before here, but I’ll summarize again because it’s important.

The SBA guarantee means that if you default on your loan, the SBA will reimburse your lender for a previously agreed upon percentage (usually 75%). When the lender gets that money, it does nothing to reduce the balance owed by the borrower and/or guarantors.

Borrowers who are often shocked (and confused) at the revelation that they are on the hook for 100% of the loan balance. “Why did I pay all that money for the SBA guarantee!” they exclaim.

Good question.

The value of the SBA guarantee is in getting the loan in the first place. I realize it feels pretty worthless once you’ve defaulted, but the whole premise of the SBA loan program is to give loans to people who can’t get them through traditional channels. In order to fund the SBA program, the SBA charges borrowers a guarantee fee.

I wish they’d call it something else, because “guarantee fee” is a confusing term, especially when a borrower is signing all sorts of documents, including a “personal guarantee”. It’s easy to see why some small business owners get confused.

If they don’t change the name, at very least they should add a disclaimer somewhere in the loan documentation (preferably in bold and underlined) that makes it abundantly clear: if you default on this loan, the SBA guarantee will not reduce the amount you owe. The guarantee is for the lender only.

SBA Gets the Final Say on Any Settlement

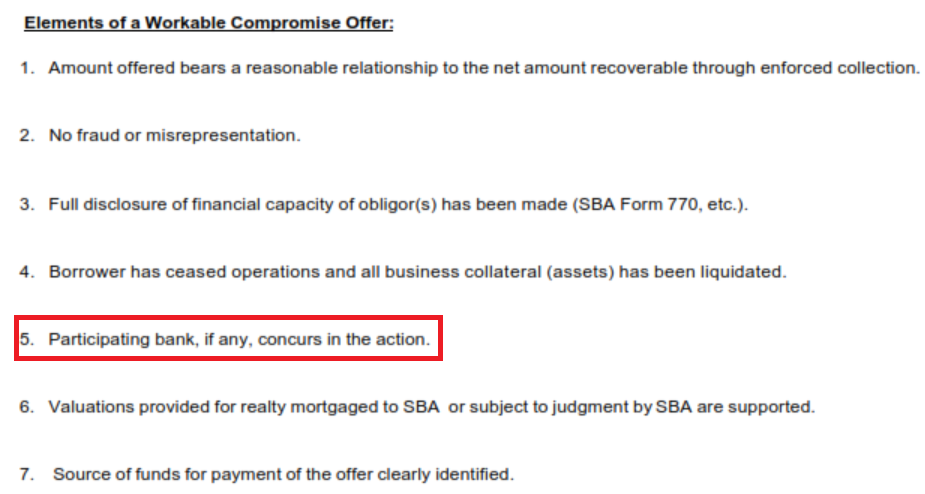

It’s always beneficial to have a good relationship with your lender, because you do need to have their support. Again referring back to the initial screenshot, I call your attention to workable element #5. “Participating bank, if any, concurs in the action.”

But that’s not the end of the story.

Even if the bank is in your corner, it’s the SBA’s decision that matters most. They can override a banks recommendation and there isn’t much that can be done to change it (unless there is an egregious mistake or misunderstanding).

But can’t the lender just settle the loan anyway?

They could. Technically they are the lender, not the SBA. But chances are that they won’t.

The reason is simple: if your lender forgives the loan without SBA approval, they risk losing the guarantee.

The math on that one is easy. Get reimbursed for 75% of the loan balance, or recover significantly less by defying them. Like I said, a no-brainer for the bank.

Conclusion

I hope that this article hasn’t discouraged you. That’s certainly not my intent. SBA loan forgiveness is possible. You just need to understand the rules of the game. If you’d like to schedule a case evaluation, you can choose a date and time here. We’ll discuss your SBA loan situation, and I’ll lay out your options.