After you do something for a while, patterns begin to emerge. So naturally, after working with hundreds of small business owners who are in the midst of SBA default for the past 9 years, some recurring mistakes have emerged. I’m writing this article in hopes that if you can’t afford to pay your SBA loan, that you’ll use this guide to avoid making these common mistakes.

Avoiding Your Lender

It’s certainly stressful to watch your business crumble in front of your eyes. But when your banker is calling or emailing you to see why you have missed your payment(s), you need to be responsive. If you duck their calls for a long enough period of time, you are inviting problems. They’ll either refer it to their attorney to start litigation, or to close their file, and refer to the SBA. If you also ignore the SBA, the file will end up at the treasury, where SBA loans go to die.

Taking On Debt To Save Your Sinking Ship

Your business is running a cash flow deficit each and every month. Not because the business is growing, but because it’s simply not profitable. Rather than taking a good hard look at the viability of their business, many owners turn to credit cards, their 401k, or their home equity loan. I’m not saying that your business isn’t worth fighting for. But there needs to come a time when you look in the mirror and ask yourself “is this business viable?”. If you don’t know the answer, you’d better find out, and quickly. It’s only going to make matters worse if you max out your credit cards, only to close the business anyway.

Holding On Too Long

You haven’t taken a paycheck for yourself in….well, actually you can’t even remember the last time you took a paycheck. The business hasn’t turned a profit since you opened. Any yet, you consider yourself a gritty business owner that is going to fight tooth and nail to make it work. But here’s the thing about grit: it’s not always a good thing. Not letting go of a failing business when you really should can really backfire on you. If you accumulate debt and deplete all your savings all in the name of saving the business, it could really hamper your chances of a successful SBA Offer In Compromise

Putting Every Last Dollar You Have Into The Business

This goes hand-in-hand with holding onto your failing business for too long. I occasionally get a phone call from a borrower who tells me that their business is going to close, and they need help settling. “Great, that’s exactly what I do”, I tell them. “So, if the bank and SBA were willing to settle, where would you get the funds to settle with?”. Their response? “Oh, I have nothing left, I put it all into the business. I was hoping to claim financial hardship.” So here’s the thing about that: neither your lender or SBA release personal guarantees in exchange for nothing. That’s simply not how these negotiations work. If you expect to settle, you need to go in expecting to pony up some cash. So if you are thinking you may have to go down this road, be sure and make that decision before all the cash dries up.

Selling Business Assets Without Permission

Sometimes this comes in the form of an honest mistake, sometimes it’s done intentionally, with the business owner knowing full well that the bank and SBA would not appreciate it, and that the loan documents prohibit it. Either way, if you sell the business assets without the permission of your lender, you are setting yourself up for make problems

Fraudulently Selling The Business Or Business Assets

If your world is collapsing, it can be tempting to cut some corners. “The bank will screw me if they have the chance, so I’m just playing their game” is often the rationale. Borrowers have articulated to me that they are simply doing what they need to do to survive. And in some cases, apparently that includes committing fraud. I’ve written about this before, and my bottom line is that when you defraud a lender, you are crossing a line. There is a major difference between being a smart business owners and fraud. Selling your business or business assets to a friend, family member, or business associate with the intention of buying them back later, then lying about the nature of the transaction is not a legitimate strategy.

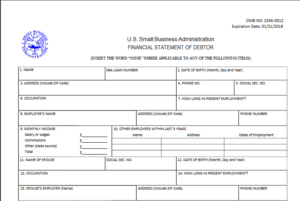

Omitting Information From SBA Form 770 (SBA Personal Financial Statement for the OIC)

Everyone understands what the SBA wants from you (pro-tip: money). Over the past 9 years that I’ve been assisting borrowers with the SBA Offer In Compromise, I’ve come across more than one clients that sense that they have something that the bank or SBA wants, so they conveniently “forget” to include certain liquid investments like IRA and 401Ks or investment properties. As part of the process, bank’s run your credit report and if they see a mortgage, they’ll know you own a property. No mortgage? They can just as easily run your name through tax records.

Once a bank catches you with your hand in the cookie jar, you will lose a valuable asset: trust. Every interaction after you get caught omitting material information will be entered into with the belief that you are a liar. Not ideal to successful settle.

Assuming Bankruptcy Is Your Only Option

My general view in life is that there is never one option that makes sense for everyone. The same applies to dealing with SBA default and SBA Offer In Compromise. I’m not even going to make a case for why you should attempt to settle, because that’s not my point. My point is that there are alternatives to bankruptcy, and submitting an Offer In Compromise is one of them. Take out the old yellow legal pad and make a “pros and cons” list. For some, settling makes sense, for others, it may be bankruptcy. But before you choose your path, make sure you understand all the angles so you can make an informed decision. Talk to a guy like me, talk to a bankruptcy attorney, then you’ll be in a position to make a decision you feel confident in.

Not Understanding What You Signed Up For As An SBA Loan Personal Guarantor

This actually happened just last week. My new client needs to settle two SBA loans. According to him, he had nothing to do with any of it. His ex-girlfriend opened a store, and needed his good credit. He swears to me that he asked the banker to confirm that if she defaulted, it would only come back to the business. He says that’s what the banker told him. Obviously I wasn’t there so I don’t know for sure how that conversation went, but his story underscores and important point. If you sign ANY legal document, ask a legal professional to review it, and confirm exactly what it means.

Submitting An Incomplete SBA Offer In Compromise Package

Look guys, I totally understand the desire to want to get the entire SBA Offer In Compromise process over with. Every moment you deal with it, you feel the heartache of losing your time, your money, and your business. But you need to focus until we cross the finish. After that, feel free to take a nice long nap. Focus means making it very easy for your bank and the SBA to understand your personal financial situation. Common errors are missing pages of tax returns, screen shots of your bank account rather than actual statements, leaving entire sections of the PFS blank, and “ball parking: your monthly expenses. Show them that you are talking this process very seriously. After all, if you don’t take your Offer In Compromise seriously, why would the bank or the SBA?

Getting Aggressive With The Bank

A handful of my past clients believed that the successful negotiation of their settlement required aggression. I think they expected it to be like a movie. I’d pound on the table, throw a chair, or verbally dress down my adversary. Basically fight with them until then bent to my will. In reality, SBA settlement negotiations are typically not like that. I can definitely tell you that you get better outcomes when you are friendly and respectful. It’s 100% possible to negotiate a great settlement without have to resort to getting nasty. Just think about it: would you be more willing to help a person who is nasty and mean, or a person who is friendly and helpful. Well guess what? Workout officers are people too!

Having Unrealistic Expectations About Amount You Can Settle For

Settlements are based on facts. It’s not about low balling, misdirection, or throwing an offer against the wall and hoping it sticks. Many borrowers arbitrarily choose how much they are offering to settle. In reality, determining the amount of your offer is anything but arbitrary. It should be based on your personal financial situation. And if your personal situation is weak, keep in mind that the SBA will not release your personal guarantee in exchange for nothing.

Making Unproductive Arguments

By far, the most common unproductive argument my clients ask me to make goes something like this.

“I lost a lot of my money on this business, the bank is getting most of their money back (by way of the SBA guarantee) and I paid thousands of dollars of interest on this loan. They should be willing to release me.”

Sorry, but none of those arguments will move you closer to your ultimate goal. The bank is owed money, and how much you lost is not going to impact their desire to recover as much money as possible. Neither is the fact that the SBA reimbursed the bank, since all that really means is that the SBA stands to lose majority of the money.

Expecting Pity

I once had a woman email me. She had unsuccessfully attempted to settle her SBA loan by herself before reaching out to me. The SBA swiftly declined her OIC for one simple reason: she asked to be released in exchange for nothing. Instead of offering even a small sum, this woman had tried a different course of action. She sought pity. I don’t recall her exact words, but her rationale went something like this:

“I’m just one small fish in a giant ocean. The SBA has millions and millions of loans, and I’m so small that I barely even exist. So won’t you let this little fish swim away?”

The mistake here is obvious. She assumed that the SBA would read her story, feel bad, and released her from her personal guarantee. Any offer you make should be based on the facts and figures that are reflected in your financial documents. Forget about appealing to their humanity.

Not Understanding How The SBA Guarantee Works

When you are trying to sell something, you need to understand who you are selling to. When a guarantor attempts to settle their defaulted SBA loan, some guarantors invoke a false argument. Since the SBA reimburses the bank for a large portion of the loan (usually 75% for 7a loans), they reason, all they need to do is offer the remaining 25%. The misunderstood part is that just because the SBA reimburses the lender, it doesn’t mean that the debt goes away. The SBA still wants their money back. Your offer needs to be based on your ability to pay. How much the SBA reimburses the bank for is irrelevant, and unrelated to the amount you pay to settle your SBA default.

Trying To Go Over Your Bank’s Head

It’s never easy to deal with a difficult bank. Slow response times. Short or cryptic email responses to direct questions. And of course, a declined OIC. In situations like this, a guarantors instinct is to seek a lifeline. The natural place to turn in this case SEEMS like the SBA. But it’s not. The SBA pays lenders a servicing fee. Until the bank closes its file on you, the SBA expects the lender to handle all servicing matters. This includes evaluation and decision on an Offer In Compromise. Unless something egregious is going on, the SBA invariably declines to get involved, and will defer to your lender. In order words, they’ll say “sorry, you need to talk to your lender”.

Underestimating the Value of Your Home

It’s funny how things work out. When borrowers apply for a residential mortgage or home equity loan, they always complain when the appraisal comes in lower than expected. “No way!” protests the borrower, “my home is worth at least $100,000 more than that!” But when the tables are turned, I hear reactions that exactly the opposite. Whenever a borrower estimates the value of their home, all of sudden the house needs new roof and has a cracked foundation. We list the value of the home on the PFS, the bank orders an appraisal, and guess what happens? The value comes back HIGHER than the borrower estimated. Of course, this means there is more equity in the home than we stated. In turn, this means there is more equity. The ultimate result is that the OIC we submitted was too low, and needs to be increased. Bottom line: when you estimate your home value, be reasonable and try not to let your objective of a low settlement bias you.

Expecting Your Lender To Pay For Your Lifestyle

Section 23 of the Form 770 asks you to list your monthly fixed expenses. Some take this as a opportunity to list their country club dues, vacations, and boat payment. Sure, these are actual expenses that you actually pay for. But keep in mind what the point of this exercise is. The bank and the SBA are attempting to determine if you can afford to continue making your loan payment. Even though not explicitly stated, they are asking for your non-discretionary expenses like your mortgage payment, loan payments, utilities, and so on. When you list items that are clearly not needed, you indicate that you expect them to wait on payment while you do nothing to curtail unneeded spending. Not a great look.

Not Realizing Your (Non-Guarantor) Spouse’s Impact on an OIC

Just because your spouse didn’t guarantee the loan, it doesn’t mean they don’t play a role in your OIC. When a spouse has significant income or assets of their own, a banker could easily argue that your spouse could pay all the household expenses. That would leave your income available to make SBA loan payments.

Assuming You Have All the Time In The World

Nothing gets me more annoyed than getting a call from a borrower who got their 60 day letter 50 days ago. After carrying on with life for the better part of 2 months, they reach out to me for help. Scrambling at the last minute makes for unnecessary stress for everyone involved. I understand that not everyone is going to hire me. But if you do, make that decision well in advance of the deadline. It will reduce the stress level for all involved, and will ultimately result in a higher quality OIC package.

Still have questions? Contact me!